High cash rates no barrier to housing boom, data shows

Three Reserve Bank interest rate cuts were widely credited with accelerating growth in property values last year, but historical data shows the most drastic price surges aren’t always due to falling borrowing costs.

The 8.6 per cent increase in home values last year was the 11th strongest calendar year of the past four decades, according to data compiled by analytics firm Cotality.

Of the top five years of growth out of the past 40, only the 24.5 per cent boom in 2021 occurred with interest rates below current levels.

The strongest year of growth, when values soared more than 31 per cent in 1988, interest rates were around 15 per cent.

“Sometimes home values surge when you least expect it,” said Cotality Research Director Tim Lawless.

“These standout years remind us that housing markets are influenced by more than just interest rates. Fiscal stimulus, credit availability, migration trends and economic shocks all play a role in shaping outcomes.”

Home prices have declined in only six years in that period.

The largest dip occurred in 2008, as the Global Financial Crisis rocked the housing market, but rapid loosening in monetary policy saw values rebound by more than 10 per cent the following year.

An imbalance between supply and demand is the primary driver of price growth, with the Housing Industry Association estimating Australia’s housing shortfall is close to two million.

An uptick in building approvals in November, driven by a sharp rise in apartment projects, should translate into higher levels of home building in 2026, said HIA Senior Economist Tom Devitt.

“After nearly a decade of under-building, the foundations are finally being laid for a broader housing recovery in 2026,” he said.

On the demand side, inbound migration levels are also gradually returning to pre-COVID levels.

Net overseas migration fell to 306,000 in the past financial year, down from a peak of 556,000 in the year to September 2023, and is projected to fall further in coming years.

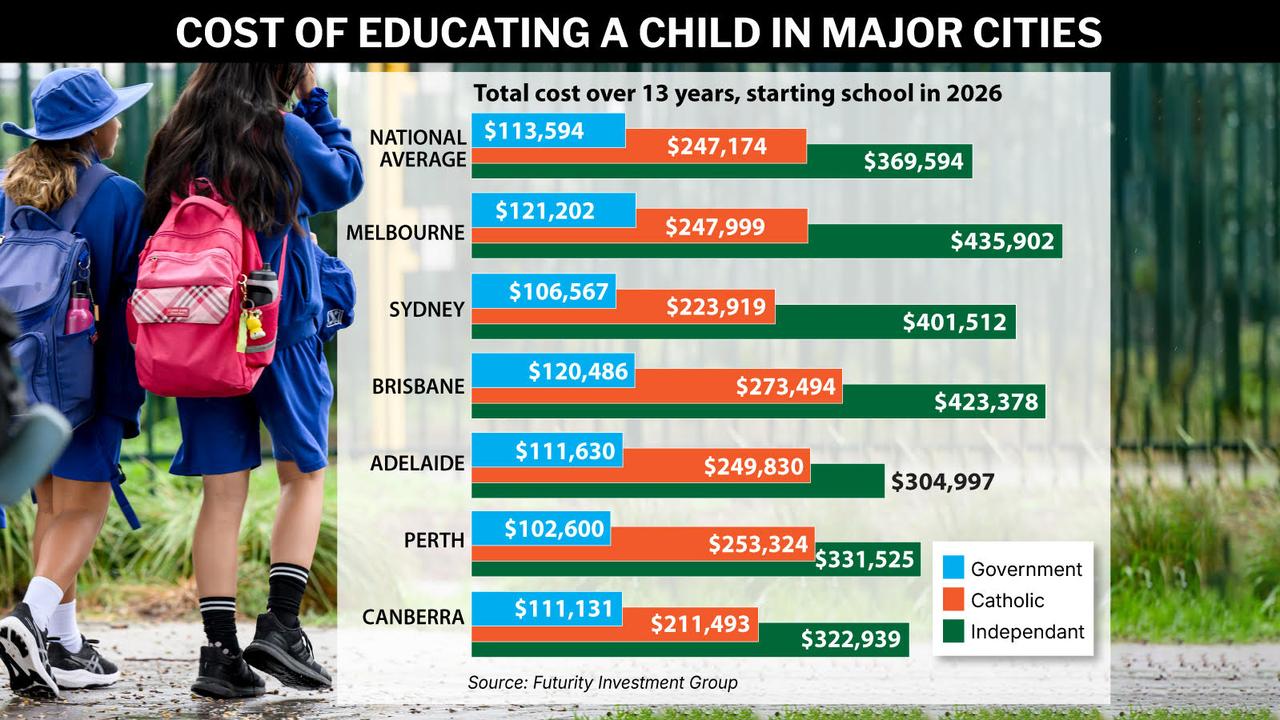

High school costs forcing indebted parents to work more

Australian families are reconsidering whether to have more children and are relying on others for help to pay for education fees as the cost of schooling accumulates.

For a child starting school in 2026, it will cost families in major cities $113,594 for a government education, $247,174 for private schooling and $369,594 to send them to an independent school over 13 years.

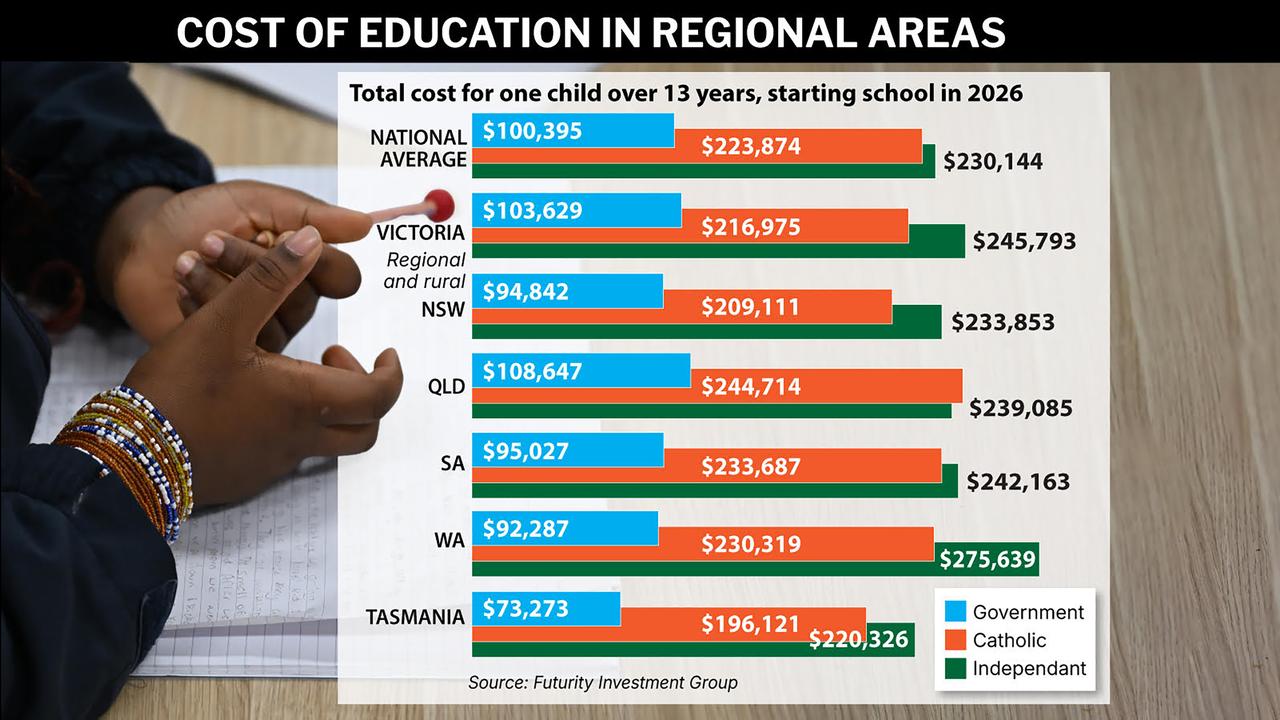

In regional and remote areas, families will pay $100,395 for a government education, $223,874 for Catholic and $230,144 for independent schools.

The research conducted by school finance group Futurity takes in school fee data from Australia’s curriculum authority and interviews with 2500 parents about their spending habits.

Melbourne topped the capital cities in government school costs at $121,202, while regional and remote Queensland parents face the steepest education bill of $108,647.

Government school fees made up 13 per cent for metro and five per cent for regional costs, with the remaining amount going to add-ons including outside tutoring, transport, school camps and uniforms.

Canberrans will spend the most for a Catholic education while in regional and remote Queenslanders pay the highest fees at $273,494.

Independent schools are most expensive in Melbourne, costing 435,902 while Western Australia is the priciest for regional and remote schools at $275,639.

Families value education, with nine in 10 saying education is important for their child to thrive in life, Futurity’s Sarah McAdie said.

“(They) are prepared to make sacrifices in order for their child to access the education that the parents choose and value for their child,” she told AAP.

But parents are increasingly looking to save by searching for second-hand school uniforms, making a laptop last longer and spending less on musical instruments and camps.

A third of respondents said they turned to credit debt, while others are having fewer family holidays and working more to afford the quality education for their kids.

Over half said they rely on others, including grandparents, to pay for their children’s education.

“Alarmingly, 45 per cent of parents said that they are now considering having less children as a result of the cost of raising and educating a child today,” Ms McAdie said.

Families have been tightening their spending as concern increases about Australian schools being fully funded, according to the Australian Council of State School Organisations.

“When the household budget is under pressure, things like sport and camps and upgrades are the first things that are scaled back,” interim chair Peter Garrigan said.

He said the real test is whether every child can participate fully without money being a barrier, as parents turn to the “bank of grandparents” for help.

“Australia’s society should be able to support everyone to do that,” Mr Garrigan said.

In Australia, 63 per cent of students are enrolled in government schools, followed by 20 per cent in Catholic schools and 17 per cent in independent schools, according to the bureau of statistics.

Cycling’s Flying Burrito aims for more Paralympic gold

In the rich, fast-food tradition of the KFC Kid, Australian track cycling now has the Flying Burrito.

And just as Ryan Bayley was a lot more than his love of fried chicken, Korey Boddington’s love of the Mexican staple belies a fierce drive and immense talent.

Boddington’s coach David Betts gave him the nickname. The Paralympic gold medallist will make as many as 40 burritos a week to help fuel his track sprinting regime.

He is the reigning Australian cyclist of the year, winning the Sir Hubert Opperman Medal, for his four titles and two world records at last year’s world track para-cycling championships.

Boddington claimed the “Oppy” 21 years after Bayley, another elite track sprinter with a relatable dietary regime, took out the award for his two Olympic gold medals.

Bayley will always be remembered as the KFC Kid, or Flyin’ Ryan. Two decades later, Boddington has embraced his moniker.

“My nutritionist, for a fair while she was trying to integrate different food,” Boddington told AAP.

“But I’m hitting all my numbers.

“Once she realised I’m really happy eating the same thing – I’m a very simple man – she’s all on board. She thinks it’s the best.”

Just like Bayley, Boddington is the real deal.

The 30-year-old won gold at the 2024 Paris Paralympics less than two years after taking up track cycling.

Then last year, he won the C3 category at the para-cycling world titles in the sprint, 1km time trial and elimination race. He also rode superbly in third wheel to clinch the win for Australia in the mixed C1-5 team sprint.

He set the C3 flying 200m world records of 10.581 seconds for the flying 200m and one minute 2.848 seconds for the kilo.

Boddington was one of the Australian para-cyclists featured in last year’s documentary Changing Track.

He is the second para-cyclist to win the Oppy, two years after Amanda Reid. Consider that other contenders for last year’s Oppy included Olympic BMX champion Saya Sakakibara, road cycling’s Grand Tour stars Jay Vine and Sarah Gigante, and track sprinter Leigh Hoffman.

At 11, Boddington suffered serious injuries to an arm when hit by a van. At 15, a motocross injury nearly killed him and left him with an acquired brain injury.

“I’ve given Mum and Dad some grey hairs, that’s for sure,” Boddington said.

He works as an accountant and will marry Chloe this year on the 10-year anniversary of when they met.

The Queenslander, who trains at the Anna Meares Velodrome in Brisbane, is aiming for the LA Games ahead of competing at home in the 2032 Paralympics.

Boddington is also pleasantly stunned at the recognition he now receives.

“I think everyone can do what I can do, but one lady said to me at the (cyclist of the year) awards, ‘No, you’re not normal’,” he said.

The “Oppy” honour roll is elite. Along with Bayley, the winners include Cadel Evans, Anna Meares, Simon Gerrans, Grace Brown and Sakakibara.

“There are huge names,” Boddington said.

“it’s very strange, because I look at Cadel and people like him – I’ve only been cycling for a bit over two years.

“I’m definitely not done. The stove top is just getting warm.

“I can’t comprehend it, but someone can, and to put me on the same level or class as them – Cadel Evans – I haven’t done anything near as much as him.

“Being given the same recognition, it’s mind-boggling. It’s bloody cool.”

With all the adversity Boddington has overcome to achieve this success, he also has a healthy dose of perspective.

“I guess over my life, having all the accidents I’ve had … that’s just the one thing I’ve realised – don’t stress the little things, life can be over like ‘that’,” he said.

“I don’t believe it (his success). I feel like an imposter, in a way, because I know how hard I’ve trained, but some people work their whole lives and don’t do what I’ve done.

“That’s all I’m focused on – training hard and going fast.”

‘Words matter’: spy chief talks up ban on hate groups

A bid to ban extremist groups following the Bondi massacre will be good for Australia, the nation’s spy chief says, as he warns there is “permission” for politically motivated violence in society.

Draft laws to be debated next week in parliament when it returns early would introduce a framework to outlaw hate groups that fall below a threshold to designate them a terrorist organisation.

Organisers, supporters and recruiters of listed groups face up to 15 years in jail and members seven.

The ability to ban groups promoting violence was welcome, ASIO director-general Mike Burgess told a parliamentary inquiry on Tuesday.

“I’ve been on the record since early two years ago … talking about how words matter, because inflamed language can lead to inflamed tension, that can lead to violence,” he said.

“We’ve certainly seen a transition and a rise of that more permission for politically motivated violence or communal violence in our society.

“We’ve unfortunately as a nation, allowed behaviours to be normalised, and when they’re normalised, they’re accepted, and that means more of them, it’s more permissible, and it can happen.”

The bid to strengthen hate speech laws are in response to an Islamic State-inspired attack on a Jewish Hanukkah celebration at Bondi Beach on December 14.

A father-son are accused of killing 15 people and injuring more than 40 others.

A national day of mourning will take place on January 22, with flags to be flown at half-mast.

Mr Burgess said the spy agency acknowledged “the deep pain and grief” of the families, friends and community of the dead and injured

“ASIO officers continue to work around the clock on this investigation,” he said.

“That’s what the families of the victims and all Australians deserve.”

Home Affairs Minister Tony Burke has indicated extremist Islamic organisation Hizb-ut Tahrir and the neo-Nazi National Socialist Network could be listed under the reforms.

The nation’s biggest neo-Nazi group will disband by midnight on Sunday to avoid jail time under the new laws.

Opposition home affairs spokesman Jonno Duniam said the nation did not want people avoiding justice by “tearing down a banner and re-emerging under a different name”.

“The Albanese government must also clarify whether this disbandment actually makes it harder to prosecute the individuals responsible for spreading hate, intimidation and extremism,” he said.

“If extremist organisations have already found a way to circumvent these new laws, then it is very alarming.”

The inquiry will hold a public hearing on Wednesday in Canberra, where it will hear from Jewish groups and human rights advocates.

A report is due by Friday before parliament returns next week to debate the reforms.

Lifeline 13 11 14

beyondblue 1300 22 4636

Lobby pressure in spotlight after festival capitulates

A prominent Jewish author says the stifling of criticism of Israel is increasing levels of anti-Semitism, as a major national festival “capitulates” and cancels its event.

Adelaide Festival has canned its Writers’ Week event following a mass boycott from authors in response to Palestinian-Australian novelist Randa Abdel-Fattah being removed from the program.

In announcing her resignation, director Louise Adler said “extreme and repressive” efforts from pro-Israel lobbyists had been behind the board decision and said it had weakened freedom of speech.

Dr Abdel-Fattah has been targeted by conservative Jewish groups for sharing posts critical of alleged Israeli war crimes in Gaza.

Independent journalist and author Antony Loewenstein, who sits on the advisory committee of the Jewish Council of Australia and has regularly appeared at the Adelaide event, said such lobbying moves were “a familiar pattern”.

“What worries me greatly is these kinds of actions are worsening anti-Semitism because what a lot of people are seeing, and I’m talking about non-Jews here, is often secretive, powerful, in my view bigoted, powerful forces trying to curtail or silence critical voices,” he told AAP.

“That leads to very unfortunate stereotypes about Jews, which is something I worry about as a Jew.”

Adelaide Festival is not the first organisation to face strong backlash after deplatforming an individual who had criticised Israel’s actions in Gaza.

A similar boycott occurred at the 2025 Bendigo Writers Festival when more than 50 writers and moderators boycotted the event over concerns its code of conduct would suppress discussion of Israel’s bombardment, with a co-curator arguing it had been subject to a lobbying campaign to remove Dr Abdel-Fattah.

The ABC unlawfully sacked journalist Antoinette Lattouf for sharing a post relating to the conflict in Gaza and was fined $150,000 as a result.

A Federal Court judge found the ABC “surrendered” to a co-ordinated email campaign against Ms Lattouf by pro-Israel lobbyists and sacrificed her for spurious reasons.

Reflecting on Dr Abdel-Fattah’s removal, Ms Lattouf urged the media to “hold its gaze” on Gaza, rather than “manufactured controversies designed to exhaust and distract”.

“It is both baffling and disheartening to watch institutions continue to bend to pro-Israel lobby pressure as the genocide intensifies, ceasefire breaches pile up, and Australia’s democracy is strained by attempts to silence criticism of these assaults,” she told AAP.

Former chair Judy Potter will return to head up a new Adelaide Festival board after its previous board members quit over the writers’ festival drama.

“We’ve had a very challenging week … we really need to wrap our arms around the Adelaide Festival as a state,” South Australian Arts Minister Andrea Michaels said.

Premier Peter Malinauskas has been accused by the Greens and arts commentators of placing pressure on the board to rescind its invitation to Dr Abdel-Fattah, a claim rejected by the Labor premier.

Central bankers defend Fed’s Powell after Trump threat

The chiefs of many of the world’s major central banks have issued a joint statement in support of Federal Reserve chair Jerome Powell , after the Trump administration threatened him with a criminal indictment.

Powell is at the centre of a US administration’s criminal probe about the renovation of the Fed’s headquarters, which he called a “pretext” to win presidential influence over interest rates.

The heads of the European Central Bank, the Bank of England, the Bank of Canada, the Reserve Bank of Australia, and eight other institutions said Powell had acted with integrity and that central bank independence was crucial for keeping prices and financial markets stable.

“We stand in full solidarity with the Federal Reserve System and its Chair Jerome H Powell,” the central bankers said in a rare joint statement on Tuesday.

“The independence of central banks is a cornerstone of price, financial and economic stability in the interest of the citizens that we serve.”

The US probe has already drawn criticism from the world of finance and also some key members of Trump’s Republican Party.

Central bankers fear that political influence over the Fed would erode trust in the bank’s commitment to its inflation target. This would lead to higher inflation and global financial market volatility.

Since the US is the world’s dominant economy, it would likely export this higher inflation via financial markets, making it more difficult for other central banks to keep prices stable.

“It is therefore critical to preserve that independence, with full respect for the rule of law and democratic accountability,” the group of central bankers said.

It included the central bank chiefs of Sweden, Denmark, Switzerland, Australia, South Korea, Brazil and France, as well as the chair of the Bank for International Settlements, an umbrella body.

A source said before the statement was published that all central bankers would be welcome to join later.

Woodside’s floating gas platform arrives off WA coast

A massive floating platform has arrived off the West Australian coast as Woodside Energy’s controversial Scarborough gas project nears production.

The 70,000-tonne floating production unit was slowly towed by five large ocean towing vessels more than 7400km from China to its position 375km off Karratha.

The journey began in November, with Woodside comparing it to the equivalent of towing an apartment block at jogging pace from Perth to Sydney and back again.

One of the largest semi-submersible facilities ever built, the floating production unit features six deck levels, 75 beds, a gym and open-plan communal living areas.

It measures 165m from keel to top, which is taller than a 50-storey building.

The unit will be used to separate, dry and compress natural gas from the initial eight wells in the Scarborough gas field once the project enters production in the second half of 2026.

The treated gas will then travel via a 430km pipeline to Woodside’s Pluto LNG plant on the Burrup Peninsula for liquefaction and export to Asia.

Having the floating production unit safely in the field was a momentous way to begin 2026, Woodside acting CEO Liz Westcott said.

“Its successful arrival is a further demonstration of the Woodside, McDermott and subcontractor teams’ collaboration and commitment to safe delivery of the project,” she said.

The Scarborough project is 91 per cent complete, Woodside says, and will provide up to eight million tonnes of LNG for export a year, as well as up to 225 terajoules of gas per day for domestic consumption.

The $18.6 billion project will boost Australia’s economy by $174 billion, support more than 3,000 jobs per year and generate $55.5 billion in direct and indirect tax payments, Woodside said.

Environmentalists have fiercely condemned the project as a potential huge contributor to climate change, saying it would generate an estimated 1.37 billion tonnes of emissions by 2055.

Woodside shares were down 1.4 per cent to $23.38 after midday on Tuesday.

US Dept of Justice probe into Fed chair sparks backlash

The Trump administration’s decision to open a criminal investigation into Federal Reserve chair Jerome Powell has drawn condemnation from former Fed chiefs and a chorus of criticism from key members of the Republican Party.

The investigation was revealed late on Sunday, US time, when Powell said the Fed had received subpoenas from the Justice Department.

It was approved and started by Jeanine Pirro, the US Attorney in Washington and an ally of President Donald Trump, according to two sources with knowledge of the investigation.

Neither Attorney General Pam Bondi nor Deputy Attorney General Todd Blanche was briefed about the decision to subpoena the Fed last week, one of the sources added.

The threat of indictment, ostensibly focused on comments Powell made to Congress about a building renovation project, sent rates on longer-term US Treasury bonds up, as investors parsed what a less independent Fed could mean for inflation and monetary policy.

If amplified, such a market reaction could constrain Trump’s efforts to reshape the Fed, considered the most influential central bank in the world and a cornerstone of the world financial system.

A rise in long-term borrowing costs could also backfire against Trump’s efforts to address broad concerns about “affordability”.

On Monday, former Fed chairs Janet Yellen, Ben Bernanke and Alan Greenspan joined with former government economic policy leaders from both political parties in raising the alarm.

“This is how monetary policy is made in emerging markets with weak institutions, with highly negative consequences for inflation and the functioning of their economies more broadly,” they wrote.

Global central bankers including the chiefs of the French and Canadian central banks publicly offered solidarity.

US Republican Senator Thom Tillis, a member of the Senate Banking Committee that vets presidential nominees for the Fed, called the move a “huge mistake” on Sunday and said he would oppose any Trump nominees to the Fed, including whoever is named to succeed Powell as central bank chief, “until this legal matter is fully resolved”.

He was joined on Monday in condemning the development by fellow Banking Committee member Kevin Cramer and Senator Lisa Murkowski, who wrote on X that “the stakes are too high to look the other way: if the Federal Reserve loses its independence, the stability of our markets and the broader economy will suffer”.

Senator Cynthia Lummis, one of Powell’s more strident critics usually, on Monday said the Justice Department’s use of a criminal statute looked like a “heavy lift” and that she did not see any criminal intent.

“We need this like we need a hole in the head,” quipped Senator John Kennedy, also on the banking committee.

Treasury Secretary Scott Bessent told Trump on Sunday the investigation “made a mess” and could be bad for financial markets, Axios reported on Monday, citing two sources.

The rise in longer-term rates notwithstanding, market reaction was relatively muted. Gold hit a record high and the dollar fell.

Major US stock indexes notched record closing highs after gains from artificial intelligence stocks and Walmart.

Powell – who was nominated by Trump to lead the Fed and confirmed in 2018 – will complete his term as Fed chief in May, but is not obligated to leave its board until 2028.

The subpoenas from the US Justice Department last week pertained to remarks Powell made to Congress over cost overruns for a $US2.5 billion (A$3.74 billion) building renovation at the Fed’s headquarters, and threatened a criminal indictment.

Powell said his testimony and the renovations were pretexts.

“The threat of criminal charges is a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the president,” he said.

Trump told NBC News on Sunday he had no knowledge of the Justice Department’s actions.

“I don’t know anything about it, but he’s certainly not very good at the Fed, and he’s not very good at building buildings,” Trump said of Powell.

Groundbreaking CEO calls time at rare earth miner Lynas

Lynas Rare Earths, a crucial player in Australia’s bid to challenge Chinese dominance in the supply chain for future technology, will lose its influential chief executive after 12 years in the role.

Amanda Lacaze announced her intention to retire from the ASX darling on Tuesday.

Easily the most prominent female CEO of a publicly-listed Australian mining company, Ms Lacaze has overseen the transformation of Lynas from little-known start-up to the only significant producer of separated rare earth materials outside of China.

“I’ve loved every day of my 12 years at Lynas,” she said in a statement released to the stock market.

“It has been a great privilege to lead the company from a troubled startup to an ASX50 company. I am extremely proud of our achievements over this time.”

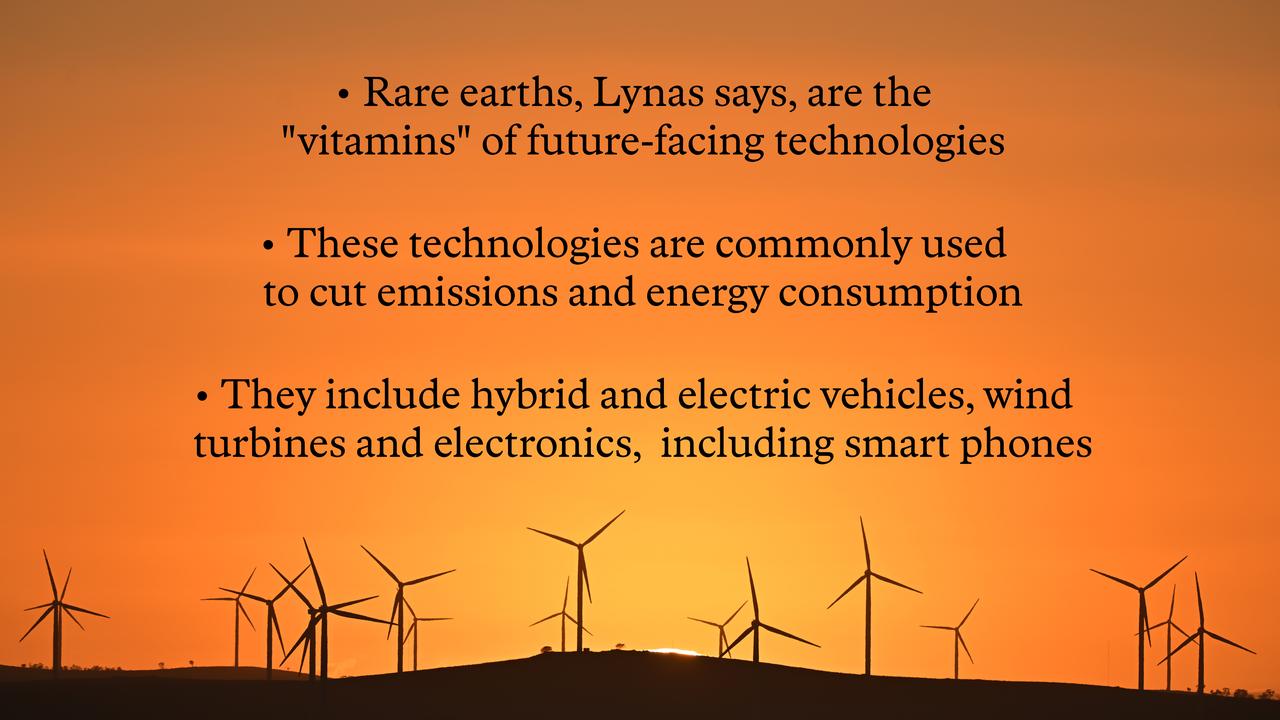

Lynas’ Mt Weld mine in Western Australia is one of the world’s most valuable deposits of rare earths elements, which are used to make permanent magnets essential to high-tech manufacturing supply chains, from fighter jets to MRI machines.

The federal government on Monday revealed rare earths, as well as antimony and gallium, would be the first critical minerals included in a taxpayer-backed strategic reserve to counter China’s stranglehold.

Ms Lacaze has been outspoken about China’s dominance and manipulation of the rare earths market, as well as the need to encourage more women into the mining industry.

“I am leaving the company in good hands with a fabulous team with unique skills and know-how, and a balance sheet to support future growth plans,” she said.

“Having successfully concluded the Lynas 2025 capital investment program and launched the Towards 2030 growth strategy, it is the right time to make this transition.”

Chair John Humphrey said Ms Lacaze had made an outstanding contribution to the rare earths industry in her time at Lynas.

“This company was in a very difficult position when Amanda took on the role of CEO. It is thanks to Amanda’s hard work, drive and tenacity that Lynas is today a leading rare earths producer and critical supplier to global manufacturing supply chains,” he said.

Lynas’ market value has increased under Ms Lacaze’s stewardship from around $400 million in 2014 to close to $15 billion.

After an initial slide, Lynas share recovered to be up more than 2.4 per cent in early trading.

The company said it will consider both internal and external candidates as it searches for a new CEO.

Ms Lacaze will remain in the role until the end of the financial year.

Dan Murphy, BWS owner’s promotions cut into bottom line

Shares in the company that owns Dan Murphy’s and BWS have hit a two-month low on news Endeavour Group is discounting to grow sales at the expense of its profit margin.

The two liquor store chains had $5.4 billion in sales in the 27 weeks to January 4, up 0.7 per cent from a similar period a year ago, Endeavour said on Tuesday.

But the group’s overall profit for the first half is expected to be between $400 million to $411 million, down from $437 million in the first half of 2024/25.

Jayne Hrdlicka, who began as the group’s new CEO on January 1 after leaving Virgin Australia, said the company made a deliberate decision to invest in lower prices to boost sales and customer engagement.

Endeavour was very pleased with the speed with which customers responded to lower prices and targeted promotional activity, she said.

Dan Murphy’s had record sales in December, with Christmas Eve setting a new daily sales record.

“The pricing and promotional decisions we have made in our retail business have generated positive sales results, delivering on our aim to better align the customer propositions for each of our brands to re-ignite top-line growth,” Ms Hrdlicka said.

“In a competitive market landscape, we have focused on reinforcing customer confidence in the value we offer across all channels, particularly in Dan Murphy’s unbeatable price and customer experience.”

Endeavour also owns more than 350 pubs across Australia, where sales were up 4.4 per cent to $1.2 billion, including a best-ever sales run in December.

“The holiday spirit across our hotels business was exceptional, enabling strong results,” Ms Hrdlicka said.

But RBC Capital Markets analyst Michael Toner said the sales update was a negative for Endeavour shares.

“In the face of structural top-line challenges and aggressive price competition in the retail liquor space, Dan’s has pulled the price lever to reinforce its value proposition,” he said.

This led to the company missing consensus earnings margin expectations by about half a percentage point.

In early trading, Endeavour Group shares were down 6.4 per cent to $3.565.