Liberal backers defend Ley as leadership showdown looms

With preparations possibly under way to roll Sussan Ley, key Liberal backers insist she will remain as leader of the opposition.

A leadership spill is shaping up for early February when parliament returns after a week of chaos that resulted in the coalition splitting for the second time since the 2025 federal election.

Conservatives Angus Taylor and Andrew Hastie are seen as the frontrunners to challenge Ms Ley.

But Liberal frontbencher and moderate Julian Leeser declared she had his “unequivocal support”.

“During this period where Australia has been in a period of national crisis, she has shown the leadership that the prime minister has failed to do,” he told Sky News on Sunday.

Asked if Mr Hastie, who has publicly spoken about his leadership ambitions, would be effective at countering rising support for One Nation, Mr Leeser replied: “Sussan Ley is our leader and Sussan Ley is the person that I support in that role.”

Liberal sources have spoken of internal anger towards Nationals leader David Littleproud for having blown up the political alliance on Thursday, which is being viewed as an act of intervention in the senior coalition party.

Mr Littleproud has repeatedly denied he demanded Ms Ley resign in a phone call during the week.

He said the three Nationals senators who resigned from the shadow cabinet after voting against Labor’s hate speech laws needed to be reinstated before the parties could reconcile.

“That’s the threshold question that our party room took,” he said.

“That’s the threshold question that was given to Sussan, she wasn’t prepared to accept it.”

By voting against Labor’s laws, an agreed position, the three senators broke the convention of shadow cabinet solidarity, triggering their resignations – which were accepted by Ms Ley.

‘Seriously wrong’: activists condemn fracking decision

Opponents of a proposed fracking project in Australia’s remote north are lining up to appeal a “failed” approval decision, as big business eyes future development of the region.

Western Australia’s Environmental Protection Authority has recommended approving the Valhalla Gas Exploration and Appraisal Program in the Canning Basin, about 120km southeast of Derby.

It could result in Bennett Resources, a subsidiary of US-based Black Mountain Energy, drilling up to 20 wells in the Fitzroy River flood plain to target fossil fuels located up to four kilometres underground.

Outraged conservation groups have vowed to appeal the regulator’s decision, with a record number of submissions expected to be lodged with investigators before a February 10 deadline.

Environs Kimberley says the community doesn’t want the region turned into Texan gas fields.

“The risk to our clean water, threatened species and the National Heritage listed Martuwarra Fitzroy River is too high,” executive director Martin Pritchard said.

“Our grounds of appeal include that the (authority) has failed to adequately assess risks to threatened species, risks to human health and social surroundings, including toxic chemicals.”

Conservation Council WA said the regulator “got it seriously wrong” but the final decision rests with WA Environment Minister Matt Swinbourn.

“It’s clear the WA community doesn’t want fracking in the Kimberley,” executive director Matt Roberts said.

The regulator has not adequately addressed the project’s potential risks, including the impact on groundwater and the stygofauna that live in it, the council said.

“By engaging with this appeals process, we hope to provide the minister with the information he needs to make the right decision,” Mr Roberts said.

Gas explorer and producer Buru Energy Limited said the authority’s recommendation for the Valhalla project was a “win” for WA and reinforced the critical role Kimberley onshore gas could play in securing its “urgent” energy needs.

“It signals to investors and the community that the Canning Basin is open for responsible, regulated energy development,” chief executive Thomas Nador said in a release to the ASX.

WA Premier Roger Cook previously said the EPA’s decision was “not a green light for fracking”.

“The EPA has made a recommendation that the particular project in question, the Valhalla Project, can have its environmental impacts managed in a way that means they are comfortable that it goes ahead,” he said.

“I suspect that decision will be appealed, so I won’t make further comment.”

Mr Swinbourn said he would consider the appeals convenor’s advice once the process was finished.

Fracking is banned in 98 per cent of WA.

However the government said its policies were “informed by an independent scientific inquiry, which said fracking could occur in WA with appropriate regulations”.

Trump threatens Canada with tariffs over any China deal

US President Donald Trump says he will impose a 100 per cent tariff on Canada if it makes a trade deal with China and warned Canadian Prime Minister Mark Carney that a deal would endanger his country.

“China will eat Canada alive, completely devour it, including the destruction of their businesses, social fabric, and general way of life,” Trump wrote on Truth Social.

“If Canada makes a deal with China, it will immediately be hit with a 100% Tariff against all Canadian goods and products coming into the U.S.A.”

Carney during a recent visit to China called the Asian superpower a “reliable and predictable partner” and in Davos encouraged European leaders to seek investment from the world’s second-largest economy.

Trump suggested that China would try to use Canada to evade US tariffs.

“If Governor Carney thinks he is going to make Canada a ‘Drop Off Port’ for China to send goods and products into the United States, he is sorely mistaken.”

Tensions between the US and Canada have grown in recent days.

Trump on Thursday withdrew an invitation for Canada to join his Board of Peace initiative aimed at resolving global conflicts.

That about-face followed Carney’s speech at the World Economic Forum in Davos, where he openly decried powerful countries using economic integration as weapons and tariffs as leverage.

‘From the heart’: Wolfe Brothers sweep Golden Guitars

Australia’s most decorated country duo were about to chase their American dream when they realised they couldn’t call the US home.

The Wolfe Brothers’ album Australian Made is a homage to the sunburnt country and the stories of its people, and on Saturday night, it helped the duo sweep the 2026 Country Music Awards of Australia.

Nick and Tom Wolfe won five of the eight Golden Guitar awards they were nominated for including the top gong for album of the year, contemporary album of the year, duo of the year, vocal collaboration of the year, and heritage song of the year at the ceremony in Tamworth.

Asked about almost moving to America, the brothers said they had made the right choice.

“This is our home, this is where our family is, this is the country we care about,” Tom told reporters after their win.

“Australian country music is from here – it’s from the heart, it’s songs about farmers, battlers, real people and us.

“Right now there is this wonderful international country music boom … the best thing for us is to do our modern type of country and sing about this place: Australia.”

The results bring the duo’s career Golden Guitar haul to 15.

Country music veteran Kasey Chambers, who had received the most nominations in 2026, won three of the 13 categories she was up for.

The Divorce Song – a collaboration with ex-husband Shane Nicholson – earned Chambers the Golden Guitar for single of the year and song of the year, while her album was awarded alt-country album of the year.

Chambers now has more than 20 Golden Guitars to her name while Nicholson has more than 15.

“I don’t think we thought we’d be standing up here together again ever,” Chambers said.

“We hadn’t written a song together since the divorce and it’s really special you (Shane) took a chance on me for this song.

“We definitely do divorce way better than we did marriage.”

Male artist of the year and new talent of the year went to Wade Forster while Max Jackson took home female artist of the year for the second year in a row.

Two-time ARIA winner Fanny Lumsden and her husband Dan Stanley Freeman won video of the year for Look At Me Now, which encapsulates the past decade and a half of her career through snippets of the life the couple share.

“This particular clip is quite different in that it’s not the world of the song, it’s the world of our lives,” Freeman said.

GOLDEN GUITAR WINNERS 2026:

FEMALE ARTIST OF THE YEAR

* Max Jackson

MALE ARTIST OF THE YEAR

* Wade Forster

ALBUM OF THE YEAR

* Australian Made – The Wolfe Brothers

SONG OF THE YEAR

* The Divorce Song – Kasey Chambers featuring Shane Nicholson

SINGLE OF THE YEAR

* The Divorce Song – Kasey Chambers featuring Shane Nicholson

VIDEO OF THE YEAR

* Look At Me Now – Fanny Lumsden

ALT COUNTRY ALBUM OF THE YEAR

* Backbone – Kasey Chambers

TRADITIONAL COUNTRY ALBUM OF THE YEAR

* Start All Over Again – Brendan Radford

HERITAGE SONG OF THE YEAR

* Australian Made – The Wolfe Brothers

VOCAL COLLABORATION OF THE YEAR

* How Many One More Times – The Wolfe Brothers with Zac & George

AAP travelled with the assistance of Tamworth Country Music Festival

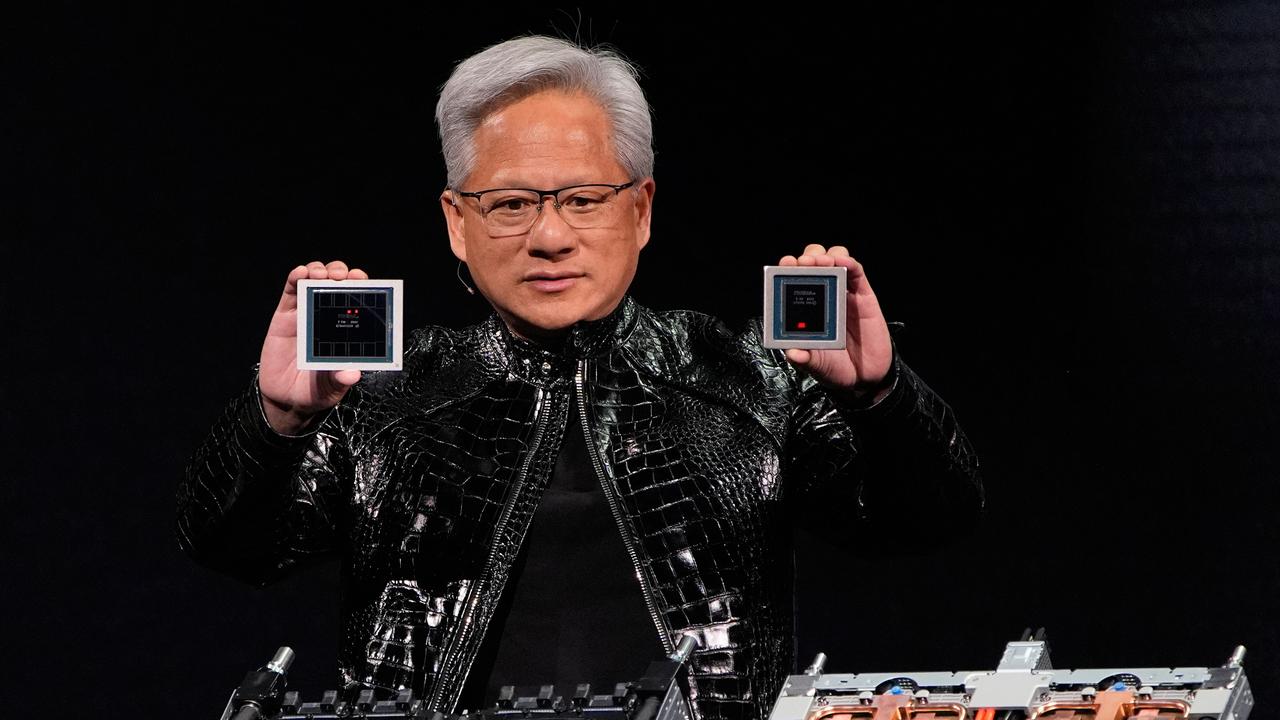

Nvidia CEO in Shanghai amid China regulatory headwinds

Nvidia CEO Jensen Huang is in Shanghai, a person briefed on the matter says, as the US chip giant faces fierce competition from local rivals and scrutiny from Chinese authorities.

The timing of Huang’s trip, to kick off annual celebrations with Nvidia’s China employees, is routine.

He is expected to attend an Nvidia party in Shanghai on Saturday before travelling to Beijing, Shenzhen and then Taiwan, another person with knowledge of the plans said.

Santa Clara, California-based Nvidia did not respond to a request for comment.

Chinese news outlet Tencent News first reported Huang’s presence in Shanghai on Friday.

Huang visited China at least three times in 2025 and met with China’s commerce minister in July.

Nvidia is waiting for Beijing to decide whether to allow the company sell its powerful H200 artificial intelligence chip to Chinese customers, a step already approved by Washington.

Chinese authorities have told customs agents the H200 chip was not permitted to enter China, people briefed on the matter told Reuters in January.

It was not clear whether this constituted a formal ban or a temporary measure.

The H200, Nvidia’s second most powerful AI chip, has emerged as one of the biggest flashpoints in US-China relations.

While demand from Chinese firms remains strong, it is unclear whether Beijing intends to ban the chip outright to support domestic chipmakers, is still deliberating restrictions or views potential measures as leverage in negotiations with Washington.

Nats’ demands complicate Liberal leadership speculation

Preparations among Liberal MPs to knife their first-ever female leader are being complicated by visceral anger towards David Littleproud for effectively demanding Sussan Ley be replaced.

A vote to roll Ms Ley is widely expected during the Liberals’ regular party room meeting when parliament returns on February 3.

Opposition defence spokesman Angus Taylor and opposition home affairs spokesman Andrew Hastie are seen as the frontrunners to replace her.

Ms Ley’s critics accuse her of a failure of leadership: for demanding parliament be recalled following the Bondi terror attack, calling Labor’s anti-hate legislation “unsalvageable” and then eventually supporting it.

But insiders are hesitant to move too quickly against Ms Ley for fear of being seen to have caved to Mr Littleproud’s demand for a new Liberal leader.

After blowing up the political alliance between the Liberals and Nationals on Thursday morning, Mr Littleproud said he would not return to the coalition while Ms Ley was leader.

“Remaining in a coalition with the Liberal party under the leadership of Sussan Ley has become untenable and cannot continue … Sussan Ley has put protecting her own leadership ahead of maintaining the coalition,” he said in a statement.

That sparked white-hot fury among Liberals, who see the comments as Mr Littleproud intervening in internal Liberal politics.

“The second he doesn’t get what he wants, he throws a tantrum,” one Liberal said of the Nationals leader.

Party sources, speaking on the condition of anonymity, said while they wanted Ms Ley gone, they were hesitant to give Mr Littleproud what he had demanded.

The anger is ultimately unlikely to deter Liberals from replacing their leader, but has made the calculus more complex, particularly for Mr Taylor, who insiders say wants to avoid blood on his hands.

The opposition defence spokesman has been holidaying in Europe, avoiding becoming embroiled in much of the drama playing out in Canberra during an emergency sitting of parliament on Monday and Tuesday.

Mr Hastie, who is based in Western Australia and has young children, must also decide whether he’s prepared to embrace the hectic travel schedule of a party leader.

Moderate Melbourne MP Tim Wilson is also believed to be considering a tilt for either the leader or deputy position.

AAP has been told contenders are holding conversations to gauge support in the party room.

Ms Ley has remained defiant, despite the flood of criticism.

Asked on Thursday if she would survive as opposition leader, she said she would.

Liberals also said Nationals leader David Littleproud might need to be axed to provide a “reset” and allow the two coalition parties to reunite.

Australians on edge as heatwave, fires, cyclone brew

A heatwave has two states on high alert for bushfires as another braces for a tropical cyclone to make landfall.

Total fire bans have been declared across South Australia and Victoria on Saturday, with temperatures in the coming days to rival those recorded in the Black Summer of 2019-20.

SA’s Yorke and Eastern Eyre peninsulas face catastrophic fire danger, making blazes almost impossible to contain if they break out.

Major fires will test the state’s firefighting capabilities, SA Country Fire Service chief officer Brett Loughlin warned.

“In those sorts of circumstances, not everyone will see a fire truck, not every call to triple zero will get the response that you would normally see,” he told reporters.

Victoria is forecast to record temperatures between 38C and 44C statewide, with wind gusts expected to peak at 70km/hr in some areas.

The mercury in Adelaide is predicted to peak at 43C, while Melbourne is set to top 40C.

Play at the Australian Open on the four largest courts will start an hour earlier to beat the heat, while the Tour Down Under’s iconic Willunga Hill stage has been dropped due to the bushfire danger.

Bushfires at Walwa and Dargo in northeast Victoria that were sparked on January 9 in scorching conditions are still burning at watch and act level.

There was potential for new fires to start and spread quickly in forecast conditions, Victorian CFA chief officer Jason Heffernan said.

“We understand it is a long weekend, and many Victorians will be enjoying the great outdoors,” he said.

“But we will be declaring several total fire bans over the course of this heatwave event and with that comes shared responsibility.”

Shallow winds will bring some reprieve to Australia’s southeast from Saturday afternoon, with the mercury set to rise again from Monday.

Parts of Victoria will edge towards 50C on Tuesday, with a forecast top of 48C at Ouyen, about 400km northwest of Melbourne.

That’s 0.8C off the state temperature record, set on Black Saturday in 2009.

Moderate fire danger ratings are in place across inland NSW, with extreme ratings expected in the Northern Slopes and Central Ranges from Monday.

Temperatures in Dubbo will hover in the low-to-mid 40s over the next week, with similar conditions across the regions.

People in a remote area east of the Western Australian town of Mandurah were told to flee on Friday evening as bushfires burned at emergency level.

Off the coast of northern WA, a tropical low was forecast to become a category one tropical cyclone.

It will be named Tropical Cyclone Luana and is tipped to intensify to a category two on Saturday morning, before likely crossing between Broome and Kuri Bay.

Communities in the warning area have been told to prepare for potential wind gusts up to 130km/h, heavy rain, flash flooding and dangerous storm tides.

Leader wins second term to rule Vietnam through to 2030

Vietnam’s top leader To Lam was appointed as head of the ruling Communist Party for the next five years, state media reports.

He pledged to turbocharge growth in the export-reliant nation.

In the one-party state, Lam was re-elected “unanimously” to the country’s most powerful job by 180 party officials from a newly-formed committee at the end of the five-yearly party congress, according to the Vietnam News Agency, citing a press release from the party.

At a press conference being prepared to conclude the party congress, Lam’s name appeared under the title general secretary, and an official confirmed the party leader would be speaking.

During his brief prior stint as party chief since mid-2024, Lam presided over fast growth underpinned by sweeping reforms that won him strong support but also criticism, as tens of thousands of civil servants lost their jobs while he promoted faster decision-making and less red tape.

Aware of the discontent stirred by those reforms, Lam moved early to secure support from rival factions within the party, including the powerful military, according to officials familiar with the process.

As concerns mounted about his plans to bolster private conglomerates at the expense of state-owned firms, Lam issued a directive ahead of the party congress underscoring the “leading role” of state enterprises, which include army-controlled telecom and defence giant Viettel.

“He normally meticulously prepares for his moves,” said Le Hong Hiep, senior fellow at the ISEAS Yusof Ishak Institute, noting that Lam, as state security minister, manoeuvred deftly to reach the apex of Vietnam’s political system in 2024 when his late predecessor Nguyen Phu Trong was facing prolonged health issues.

Lam’s re-election as party chief sends a reassuring message to foreign investors who regularly cite political stability as a key factor in Vietnam’s appeal.

Lam, 68, is also seeking to become president, with a decision expected to be announced later.

But Hiep cautioned that Lam’s bid to combine the two top roles — a system resembling the model under Xi Jinping in neighbouring China — “could pose risks to Vietnam’s political system,” which has traditionally depended on collective leadership and internal checks.

Earlier this week, addressing congress delegates seated in red-upholstered seats in a red-carpeted conference hall under a towering statue of party’s founder Ho Chi Minh, Lam promised annual growth above 10 per cent through the decade.

It’s an ambitious target which differs from World Bank’s forecasts of an average 6.5 per cent yearly expansion this year and next.

Lam wants to achieve that by changing the country’s growth model, which has hinged for decades on cheap labour and exports, turning the Southeast Asian nation into a high-middle income economy by 2030 thanks to a boost in innovation and efficiency.

In his first months as party chief, he launched the most comprehensive overhaul of the country’s public administration and government in decades, and has promised to continue with his reform drive, despite concerns over financial risks, controversial infrastructure and favouritism.

Death toll in Iran protest crackdown is 5000

The death toll in Iran’s bloody crackdown on nationwide protests has reached at least 5000 people killed, activists say, warning many more were feared dead as the most comprehensive internet blackout in the country’s history crossed the two-week mark.

The challenge of getting information out of Iran persists after authorities cut off internet access on January 8.

Tensions are rising between the United States and Iran as an American aircraft carrier group moves closer to the Middle East — a force US President Donald Trump likened to an “armada” in comments to journalists late on Thursday.

The US-based Human Rights Activists News Agency offered the death toll, saying 4716 were demonstrators, 203 were government-affiliated, 43 were children and 40 were civilians not taking part in the protests.

It added that more than 26,800 people had been detained in a widening arrest campaign by authorities.

The group’s figures have been accurate in previous unrest in Iran and rely on a network of activists in Iran to verify deaths.

That death toll exceeds that of any other round of protest or unrest in Iran in decades, and recalls the chaos surrounding Iran’s 1979 Islamic Revolution.

Iran’s government offered its first death toll on Wednesday, saying 3117 people were killed.

It added that 2427 of the dead in the demonstrations, which began on December 28, were civilians and security forces, with the rest being “terrorists”.

Iran’s theocracy in the past has undercounted or not reported fatalities from unrest.

The Associated Press has been unable to independently assess the death toll, in part due to authorities cutting access to the internet and blocking international calls into the country.

Iran also reportedly has limited journalists’ ability locally to report on the aftermath, instead repeatedly airing claims on state television that refer to demonstrators as “rioters” motivated by America and Israel, without offering evidence to support the allegation.

The new toll comes as tensions remain high over Trump laying down two red lines over the protests — the killing of peaceful demonstrators and Tehran conducting mass executions.

Iran’s attorney general and others have called some of those being held “mohareb” — or “enemies of God”.

That charge carries the death penalty.

It had been used along with others to carry out mass executions in 1988 that reportedly killed at least 5000 people.

Safety warnings as ‘heat dome’ looms over long weekend

Millions of people are bracing for severe heat over the Australia Day long weekend, with swimmers warned of threats above and below the waves.

A “heat dome” could bring record-breaking temperatures and fire danger to parts of the nation, Bureau of Meteorology senior meteorologist Kevin Parkin said.

South Australia is first in the firing line as heatwave conditions drift eastwards, bringing 40C days to capitals along Australia’s southeast.

Temperatures will start to build across Victoria, inland NSW, the ACT and southern Queensland from Saturday and into next week.

As thousands of people flock to beaches and inland waterways to escape the heat, authorities are bracing for heightened water safety risks.

It has been a busy start to summer for Victoria’s Water Police Squad, which has conducted about 500 rescues and issued some 280 infringement notices.

Boat and jet ski collisions account for most callouts, with Water Police Squad Inspector James Dalton noting there have been some “really significant” injuries.

“People need to remember that a split-second decision can have lifelong consequences,” Insp Dalton told reporters on Friday.

Threats will extend below the surf, with thousands of lion’s mane jellyfish spotted around Melbourne’s inner-city beaches.

Swimmers have been urged to cover up or else avoid the water altogether as lifesavers brace for painful stings.

Meanwhile, Sydneysiders are on guard against a more menacing predator following four recent shark attacks along the NSW coast.

The city’s popular northern beaches are expected to reopen for the long weekend after closing following the attacks.

Lifeguards will conduct regular patrols supported by jet ski patrols, increased aerial surveillance and extra drumlines to protect swimmers.

Drowning poses an even greater risk, having claimed nearly 50 lives since the summer began.

Beachgoers are urged to remain between the flags with coastal drownings three times as common around public holidays, according to Surf Life Saving Australia.

The risk extends to inland waterways, where calm surfaces can conceal strong currents, sudden drop-offs and poor visibility.

Temperatures in coming days will rival those recorded in the Black Summer of 2019-20, threatening to break all-time records, senior meteorologist Jonathan How told AAP.

High heat will result from the same slow-moving mass of hot air that brought temperatures nearing 50C to parts of Western Australia this week.

Shallow winds will bring some reprieve to the southeast from Saturday afternoon, with the mercury set to rise again from Monday.

Extreme fire danger ratings are in place across parts of South Australia with a catastrophic rating due for the Yorke Peninsula on Saturday.

Adelaide is forecast to hit 42C, while Maitland on the peninsula could reach 44C.

Moderate fire danger ratings are in place across inland NSW, with extreme ratings expected in the Northern Slopes and Central Ranges from Monday.

Sydney is forecast to reach 33C on Sunday, with elevated heat continuing into next week.

Temperatures in Dubbo will hover in the low-to-mid 40s over the next week, with similar conditions across the regions.

Melbourne is set to reach 40C on Saturday, before topping 41C on Tuesday after a brief reprieve on Sunday.

Parts of the state will edge towards 50C, with a forecast top of 47C in Hopetoun, about 400km northwest of Melbourne.

Winds across the state over the next week are forecast to be lower than those behind the fast-moving fires earlier in January.

But Mr How described this as a “double-edged sword”, posing a lower spread risk for fires but meaning high temperatures will likely persist for longer.

Victoria will be covered by total fire bans from Saturday, prohibiting all open air burns.

Total fire bans are already in place across parts of SA.