Peru election shows no appetite to tackle illegal mines

Peruvians are heading to the polls to elect a new president and Congress, but illegal mining — a major driver of deforestation and mercury pollution — has received little attention on the campaign trail, even as it spreads deeper into the Amazon rainforest and indigenous territories.

Experts warn the gap reflects a broader failure to confront what has become the country’s largest illicit economy, with major consequences for the environment, public health and indigenous communities.

“Political parties don’t understand that illegal mining has become the country’s main criminal activity and the one that moves the most money,” environmental lawyer César Ipenza said.

“There is either ignorance about what this represents for the country — or, in some cases, parties are already part of this economy.”

According to projections by the Peruvian Institute of Economics, illegal mining generated more than $US11.5 billion ($A16.3 billion) in 2025 and over 100 tons of gold exports — rivalling the formal sector and surpassing drug trafficking.

Some political candidates’ proposals, including former ministers and technocratic candidates such as Jorge Nieto and Alfonso López Chau, include measures such as gold traceability, financial intelligence and protections for environmental defenders, but these remain fragmented and fall short of a comprehensive strategy.

Others — including candidates from influential conservative and populist parties, such as Keiko Fujimori, Rafael López Aliaga and César Acuña — focus on security, economic growth or extractive development without directly addressing illegal mining or its links to corruption and territorial control in the Amazon.

In some cases — including those of Ricardo Belmont and Carlos Álvarez, both media figures turned political candidates — plans omit the issue entirely.

“Illegal mining and illicit economies are not being prioritised in government plans,” said Magaly Ávila, director of environmental governance at Proetica, a Peruvian anti-corruption group, noting that around 64 per cent of party platforms fail to meaningfully address the issue, while only about five per cent do so “clearly and explicitly”.

A March analysis by Peru’s Observatory of Illegal Mining reinforces those concerns, finding that only 12 of 36 registered political parties present specific proposals, while others offer only general statements without concrete measures or do not address the issue at all.

Peruvian authorities have previously announced operations and strategies to combat illegal mining, though experts say enforcement remains limited.

The Associated Press contacted several government entities for comment on the issue of illegal mining and indigenous protections, but did not receive a response by the time of publication.

Peruvian MPs have repeatedly extended a temporary registry that allows informal miners to continue operating while seeking formalisation, a system critics say has been widely abused and has helped illegal mining expand.

At the same time, recent legislative changes have undermined the capacity of prosecutors and judges to pursue organised crime, including illegal mining networks, according to rights groups.

Analysts say the measures reflect political pressure from small-scale miners, who have staged protests to demand looser regulations, complicating efforts to tighten enforcement.

The protests appear highly organised, suggesting the involvement of more powerful actors behind the scenes, said Julia Urrunaga, Peru program director at the Environmental Investigation Agency (EIA).

Illegal mining has grown rapidly in recent years, fuelled by soaring gold prices, which have climbed to around $US4,500 ($A6,372) to $US5,000 ($A7,080) per ounce — making even small amounts of gold highly valuable.

Once concentrated in regions such as Madre de Dios, the activity has spread into other parts of the Amazon and beyond.

“The price of gold has reached historic highs, and that has obviously driven illegal mining to expand,” Ipenza said.

“The state does not have the capacity to respond or pursue this activity.”

Illegal mining operations often rely on mercury to extract gold, contaminating rivers and entering the food chain through fish.

“In Amazonian river communities, between 50 per cent and 70 per cent of the diet is fish,” said Mariano Castro, Peru’s former vice minister of environment.

“So exposure increases exponentially, and mercury is highly toxic, with serious neurological impacts.”

Environmental and health experts warn contamination in some regions already exceeds safety standards, posing long-term risks.

Expected expansion throughout the Amazon “will bring contamination, transnational criminal groups and direct impacts on indigenous and local populations,” Ipenza said.

Illegal mining already “puts at risk our health, biodiversity and ways of life,” said Tabea Casique, a board member of AIDESEP, Peru’s largest Indigenous organisation.

“Most political parties are not taking this problem into account or presenting concrete proposals,” she said.

Former vice minister Castro called state efforts “insufficient” and said MPs have also weakened legal tools to prosecute illegal mining, including reducing penalties and limiting the ability to treat such operations as organised crime.

Gaps in oversight allow illegally mined gold to enter legal supply chains, often through processing plants where it is laundered.

Ipenza called for the government to better control small-scale processing plants and for stronger coordination across government agencies — including customs, financial intelligence units and prosecutors — to track gold flows and identify illegal activity.

Analysts say weak traceability systems are a central vulnerability.

“There is no real way to trace mining production in Peru,” said EIA’s Urrunaga.

“Authorities hold fragmented pieces of information, but there is no system — and apparently no political will — to connect them.”

“We are talking about more than $US12 billion ($A17 billion) in illegal gold exports,” she added.

“How can this be happening in almost total impunity?”

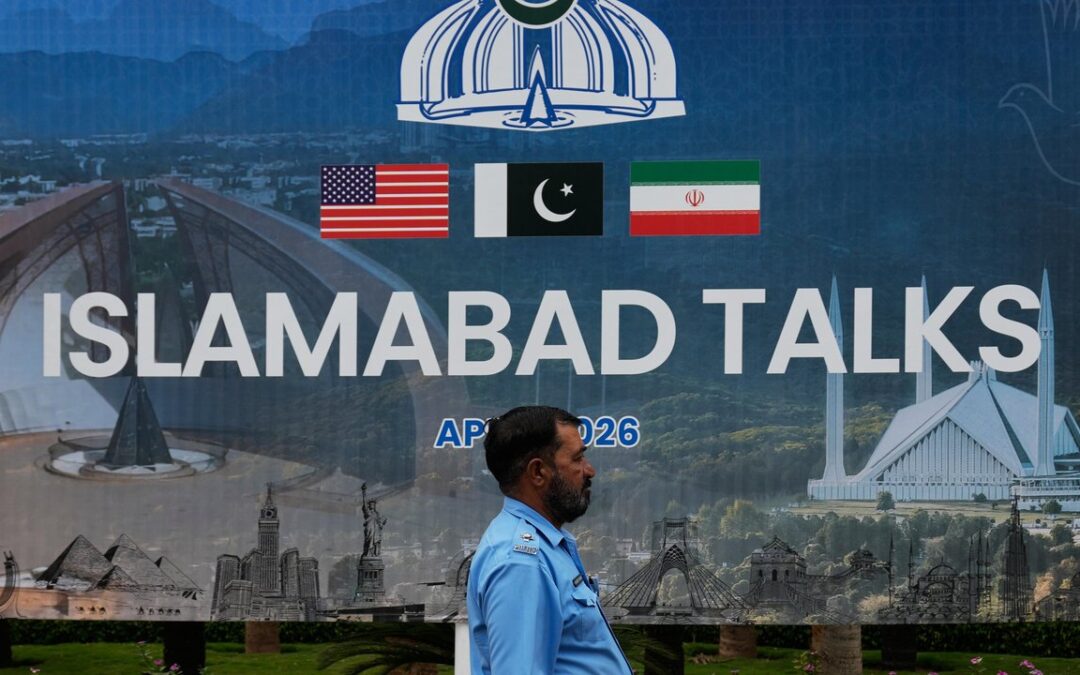

Iran set for peace talks but doubts emerge over Lebanon

The United States and Iran are to hold negotiations in the Pakistani capital Islamabad to end their six-week-old war although Tehran threw the talks into doubt by saying they could not begin without commitments on Lebanon and sanctions.

The US delegation, led by Vice President JD Vance and including President Donald Trump’s special envoy Steve Witkoff and son-in-law Jared Kushner, arrived in Islamabad on Saturday after a refuelling stop in Paris.

The Iranian delegation, led by parliamentary Speaker Mohammad Baqer Qalibaf and Foreign Minister Abbas Araqchi, arrived on Friday.

In a post on X, Qalibaf said Washington had previously agreed to unblock Iranian assets and to a ceasefire in Lebanon, where Israeli attacks on Iran-backed Hezbollah militants have killed almost 2000 people since March.

He said talks would not start until those pledges were fulfilled.

Israel and the US have said the Lebanon campaign is not part of the Iran-US ceasefire. Tehran insists it is.

Qalibaf said separately Iran was ready to reach a deal if Washington offered what he called a genuine agreement and granted Iran its rights, Iranian state media reported.

The White House did not immediately comment on the Iranian demands, but Trump posted on social media the only reason the Iranians were alive was to negotiate a deal.

“The Iranians don’t seem to realise they have no cards, other than a short term extortion of the World by using International Waterways. The only reason they are alive today is to negotiate!” he said.

Vance, speaking en route to Pakistan, said he expected a positive outcome but added: “If they’re going to try to play us, then they’re going to find the negotiating team is not that receptive.”

Islamabad was under an unprecedented lockdown on Saturday with thousands of paramilitary personnel and army troops on the streets.

“We have deployed multi-layer security for this event, which is based on co-ordination, intelligence and constant monitoring for zero disruption and full control,” Pakistan’s junior interior minister, Talal Chaudhry, told Reuters.

Trump on Tuesday announced a two-week ceasefire in the war, which has halted US and Israeli air strikes on Iran.

But it has not ended Iran’s blockade of the Strait of Hormuz, which has caused the biggest-ever disruption to global energy supplies, or calmed the parallel war between Israel and Iran-backed Hezbollah in Lebanon.

Israeli ambassador to the US Yechiel Leiter and his Lebanese counterpart Nada Hamadeh Moawad will hold talks in Washington on Tuesday, Israeli and Lebanese officials said, amid the conflicting accounts on what those talks would cover.

Israeli attacks continued across southern Lebanon on Friday.

One strike on a government building in the city of Nabatieh killed 13 members of Lebanon’s state security forces, President Joseph Aoun said in a statement.

Hezbollah said in a statement on its Telegram channel that it fired rocket salvos at northern Israeli towns in response.

Hours after the ceasefire was announced, Israel launched the biggest attack of the war, killing more than 350 people in surprise strikes on heavily populated areas, Lebanese authorities said.

Tehran’s agenda at the talks includes demands for major new concessions, including the end of sanctions that crippled its economy for years.

It also wants acknowledgement of its authority over the Strait of Hormuz, where it aims to collect transit fees and control access in what would amount to a huge shift in regional power.

Iran’s ships were sailing through the strait unimpeded on Friday, while those of other countries remained hemmed inside.

‘Don’t panic’: cash isn’t king when it comes to super

Ups and downs are a part of life and especially when it comes to your superannuation pool.

The past month has seen heightened volatility in financial markets, where much of Australians’ super is invested.

Some have seen their funds drop thousands of dollars since the US attacked Iran on February 28, creating a sense of panic.

The nation’s largest super fund has noticed a sharp uplift in members switching their investment options to cash by around four times the usual rate since then, as members try to curtail losses.

“It’s a smaller amount than what we saw during the ‘Liberation Day’ period, which was almost a year to the day since but it is a larger amount than normal,” AustralianSuper head of asset allocation Alistair Barker told AAP.

On April 2 last year, US President Donald Trump declared a so-called Liberation Day as he announced shock tariffs on goods imported into America.

The markets lost about 20 per cent in a very short period, prompting about 11,000 AustralianSuper members – equivalent to 12 times normal – to move their accounts into cash.

AustralianSuper, which manages more than $400 billion in retirement savings in almost four million accounts, has noticed switchers tend to be men and those aged 40 or older – both tend to have higher balances

“It can happen across all ages but we’ve seen a particular increase in switching for people aged 40 and above, and we’re also seeing a higher rate of men … relative to women,” Mr Barker said.

At the same time, members with high growth accounts, which have larger exposure to shares, might be more vulnerable to switching than those in balanced options, which hold shares, infrastructure, fixed interest and cash.

“In periods of stress, the pattern of behaviour tends to be that people will move from one of those options, which has more exposure to shares, into something like cash,” Mr Barker said.

But super experts, including industry body Super Members Council, warn individuals have a poor track record of picking the market and that switching during volatility seals losses, with long-term impacts.

Take this example provided by Australian Super, with simplified projections assuming no further super contributions are made:

A member had a balance of $100,000 on Liberation Day last year and soon after, switched from a balanced option to cash.

Three months later, they were $8000 worse off.

A year on, those losses total $11,000 and the pool is still under $100,000 because they missed the recovery.

The potential difference in about 30 years is between $26,000 and $57,000, depending on whether and when they switched back.

“What this really highlights is that whilst people are quite concerned when markets are volatile, some of the largest upward movements in markets are often in the days immediately around difficult periods,” Mr Barker said.

“We saw one of those (during the week), with the announcement that there was a likely ceasefire between the US and Iran.

“Markets bounced quite considerably (the day after).

“They might be thinking they’re missing the down-days but they’re also missing the up-days, and those up-days are quite considerable immediately after events such as the ones we experienced this time last year and now.”

So, theoretically, is there a time to panic about the markets?

Broadly, no, because the industry says it runs on products designed to ride out periods of market volatility.

“In fact, probably the biggest risk that many Australians face is keeping pace with the cost of living,” Mr Barker warned.

* This is not investment advice. Always reach out to your superannuation fund or investment advisor to discuss your individual circumstances.

Aussie firm losing bid to mine rare earths in Greenland

A stalled Australian rare-earth mining project in Greenland has been dealt a fresh blow, with authorities flagging its exploration licence won’t be renewed.

Perth junior miner Energy Transition Minerals (ETM) is suing Greenland’s government for billions after it brought in legislation in 2021 to ban uranium mining.

The move effectively halted operations starting at the Kvanefjeld site because uranium would be a by-product.

Many locals in the nearby town of Narsaq, population 1500, oppose the project based on concerns about radioactive dust and the risk of tailings leaks. The region is considered Greenland’s breadbasket.

The legal dispute is before Greenland’s high court but no hearing date has been set.

ETM, which has spent about $150 million on the project, received a draft decision in early April stating Greenland’s minerals ministry recommended rejecting its application for exploration licence renewal after the permit lapsed in December.

”For them to deny the extension … on the basis of legislation that is, by the way, still being tested through the legal proceedings … I would be ashamed if I were a Greenlandic lawmaker,” ETM managing director Daniel Mamadou told AAP.

The company said it was “blindsided” by the decision and had been planning a $10 million drilling program in 2026 to comply with regulations requiring a minimum spend on exploration activities.

Greenland’s minerals ministry department head Jorgen Hammeken-Holm dismissed the company’s accusations of game playing and insisted ETM would get a chance to respond ahead of a final decision.

”(The company) has had its application for a rare earth and uranium exploitation permit rejected twice. The reason for not extending the exploration permits lies in these two rejections, which provide the basis for not having to explore further,” he told AAP.

Asked if ETM’s only hope for the project starting was US President Donald Trump invading Greenland and lifting the uranium mining ban, Mr Mamadou laughed and said: ”No, of course not.”

”The company and I do not support any action that is illegal,” he said.

Mr Mamadou expressed frustration with the legal delays and accused government lawyers of dragging their feet, a claimed dismissed by Mr Hammeken-Holm.

”It is the court system that is running the process,” he said.

In March, an arbitration court ordered ETM to pay the Danish and Greenlandic government’s legal costs for proceedings totalling 3.1 million Euros (A$5.2 million) after it found it didn’t have the jurisdiction to hear the case.

Venture capitalists are funding the company’s legal action.

Mr Mamadou said the government’s treatment of ETM would not go unnoticed among other international miners.

”It’s a big test of (foreign) investor confidence,” he said, noting Greenland sent a delegation to a recent convention in Canada to promote itself as an investment destination.

”(They) claim Greenland is open for business … yet at the same time they take these expropriating actions against us.”

‘Won’t happen’: Singapore shuts down Aussie fuel fears

Motorists are being reassured Australia will not be cut off from its biggest fuel supplier, even if conflict in the Middle East escalates and stocks worsen.

Australia has locked in a supply deal with Singapore, one of the country’s largest providers of fuel, but the opposition has urged for the government to not be reliant on exports for petrol and diesel.

Singapore had no plans to reduce exports, Prime Minister Lawrence Wong said alongside Anthony Albanese at a joint press conference on Friday.

“We didn’t have to do so even in the darkest days of COVID, and we will not do so during this energy crisis,” Mr Wong told reporters in Singapore.

More than a quarter of all fuel imported into Australia comes from Singapore and Australia provides about one-third of the city-state’s LNG supply.

Mr Albanese and Mr Wong inked an agreement to continue trading large amounts of fuel and gas between the two nations.

The deal stated the countries would “make maximum efforts to meet each other’s energy security needs” at a time when fuel prices have surged and many service stations face shortages as the Strait of Hormuz remains shut.

It did not include any specific guarantee Australia would be at the front of the queue in the event Singapore’s refineries kept reducing output.

But Mr Wong shut down a question on whether Australia would be prioritised if exports had to be reduced if the energy crisis worsened.

“It won’t happen,” he said.

The blunt response prompted Mr Albanese to quip: “The prime minister is just as confident in private as he is in public.”

Nationals leader Matt Canavan said a crisis response was needed to address the fuel crisis, adding Australia should not be reliant on other nations and instead look to domestic solutions.

“I hope the government’s successful there, but we also clearly need to do more,” he told ABC TV.

“Why do we have to go cap in hand with Singapore, when we have a whole continent available to ourselves here that’s got plenty of oil and gas available?”

Mr Albanese said the relationship between Singapore and Australia meant they could avoid the worst of the fuel crisis.

“The best way to deal with this global crisis is indeed to work together as partners and as neighbours, and I look forward to continuing to engage with the prime minister,” he said.

Earlier on Friday, Mr Albanese toured an oil refinery and a liquefied natural gas terminal on Jurong Island, off Singapore’s southwest coast.

Both leaders also called for the strait, where one-fifth of the world’s oil supply flows through, to reopen.

Mr Albanese will return to Australia on Saturday.

NDIS overhaul uncertainty ‘deeply unsettling’

Exactly how the government will curb its spending for the rapidly growing National Disability Insurance Scheme remains up for debate as the health minister concedes “significant reform” is needed.

What this reform looks like and how the government will overhaul the way it funds Australia’s disability services could be outlined as soon as next month in Labor’s upcoming federal budget.

Health Minister Mark Butler refused on Friday to rule out introducing means testing as pressure grows to rein in the “out of control” spending.

But he did acknowledge fundamental changes would be needed to rein in its spiralling cost, which is growing at more than 10 per cent a year and well above the government’s target of between five and six per cent.

The scheme is expected to cost more than $50 billion this financial year and is projected to cost more than $100 billion annually within the next decade.

Earlier this week, some Labor MPs called for a wholesale redesign.

Tasmanian Labor senator Helen Polley urged colleagues to consider means testing the scheme, suggesting recipients who can afford it should be required to pay a co-contribution.

A similar approach has been introduced for aged care providers.

Victorian Labor senator and former infectious diseases physician Michelle Ananda-Rajah also raised concerns over money “wasted on unsustainable, poorly managed programs like the NDIS”.

Opposition NDIS spokeswoman Melissa McIntosh accused the government of being in disarray over the issue.

“My concern is the NDIS has gone from something that had vulnerable people at its heart … to something that seems to be getting really rotten at its core,” she said.

“And there is so much rorting going on within the system and the people that are suffering besides the Australian taxpayer are these really vulnerable people.”

Amid talk of reform, disability advocates say the disability community is struggling with the uncertainty.

“When reforms are framed around reducing growth rather than improving outcomes, it creates a sense that people themselves are the problem – and that’s deeply unsettling,” People With Disability Australia acting chief executive Megan Spindler-Smith wrote on social media platform X.

While remaining open to the scheme being made more financially sustainable, advocates say the overhaul shouldn’t come at the expense of critical services for vulnerable Australians.

Lifeline 13 11 14

beyondblue 1300 22 4636

US consumer prices surge as expected in March

US consumer prices increased by the most in nearly four years in March as the war with Iran boosted oil prices and the pass-through from tariffs persisted, further diminishing chances for an interest rate cut.

The Consumer Price Index jumped 0.9 per cent in March, the Labor Department’s Bureau of Labor Statistics said on Friday, the largest increase since June 2022 when prices soared in response to the Russia-Ukraine war.

Consumer prices rose 0.3 per cent in February.

In the 12 months through March, the CPI advanced 3.3 per cent after rising 2.4 per cent in February.

Economists polled by Reuters had forecast the CPI accelerating 0.9 per cent and increasing 3.3 per cent year-on-year.

The jump in consumer inflation followed after a sharp rebound in job growth in March, which suggested the labour market remained stable.

There are, however, concerns that a prolonged conflict in the Middle East could undercut the labour market, especially if households respond to high prices by pulling back spending.

The US-Israeli war with Iran has sent global crude oil prices surging more than 30 per cent, with the national average retail gasoline price breaking above $US4 a gallon for the first time in more than three years.

Though President Donald Trump on Tuesday announced a two-week ceasefire on the condition that Tehran reopen the Strait of Hormuz, the truce appeared fragile.

March’s increase only showed the immediate effects of the oil price shock, which has also raised the cost of diesel.

March’s surge underscored the affordability challenges facing consumers.

Trump romped to victory in the 2024 presidential election promising to lower prices.

Excluding the volatile food and energy components, the CPI rose 0.2 per cent in March after climbing 0.2 per cent in February.

Both core CPI and personal consumption inflation have been driven by businesses passing on some of Trump’s broad tariffs to consumers.

In the months ahead, economists expect the Middle East conflict to lift core prices through expensive jet fuel that will raise airline fares, and diesel, which will increase the cost of goods transported by road.

Prices of fertiliser and plastics, among other goods, are also expected to rise.

Firming inflation has left some economists believing the Fed would not reduce borrowing costs in 2026, a conviction that was reinforced by the release on Wednesday of minutes of the central bank’s March 17-18 policy meeting, which showed a growing group of policymakers in March felt that rate hikes might be needed.

The Fed left its benchmark overnight interest rate in the 3.50 per cent-3.75 per cent range.

Australians skipping, delaying medicines due to price

Australians are taking expired medication, skipping doses or opting to delay or not fill a prescription as the cost of living eats into their medicine cabinets.

The federal government has tried to tackle the issue by bringing down the maximum price for prescription drugs listed on its subsidy scheme to $25.

While that is said to save taxpayers more than $1 billion, 43 per cent of Australians have been prescribed medicines not subsidised, a survey commissioned by the McKell Institute has found.

As a result, almost one in five people said they could not afford medicines not listed on the Pharmaceutical Benefits Scheme.

About one in four people prescribed medicines outside the scheme said they do not buy the medications, around a third delayed purchases, while 16 per cent were forced to go without essentials to afford them.

Overall, more than one in five of those surveyed said they had delayed filling a prescription due to cost and 18 per cent did not fill it at all.

Some 15 per cent skipped a dose to make it last longer, and 12 per cent reported taking expired medication rather than filling and paying for a new scripts.

“They have to make a really hard decision between food and medicine, between something for their family or for themselves,” McKell Institute chief executive Edward Cavanough told AAP.

“It’s a bit of a wake-up call.”

Part of the problem is Australia’s slow PBS listing process.

In 2022, it took 391 days for a prescription medicine to go from being approved for use to being included on Australia’s subsidy scheme.

By comparison, it took 101 days in Japan, 121 days in Germany and 167 days in the UK.

This has worsened in recent years, widening to more than 600 days by 2025.

“We also have this flood of new and innovative medicines being approved,” Mr Cavanough said.

“It’s a really positive thing to be able to capitalise on the benefits of that.

“(But) the PBS can’t keep up.”

The government has reduced the maximum price on prescription medication multiple times since coming to office, with the PBS continually held up as a beacon of health policy by Australia’s major political players

Announcing a drug used to treat cerebral palsy was being added to the scheme on Friday, Health Minister Mark Butler again backed in the system.

“The expanded PBS listing is part of the Albanese government’s commitment to make medicines cheaper and more accessible for all Australians,” he said.

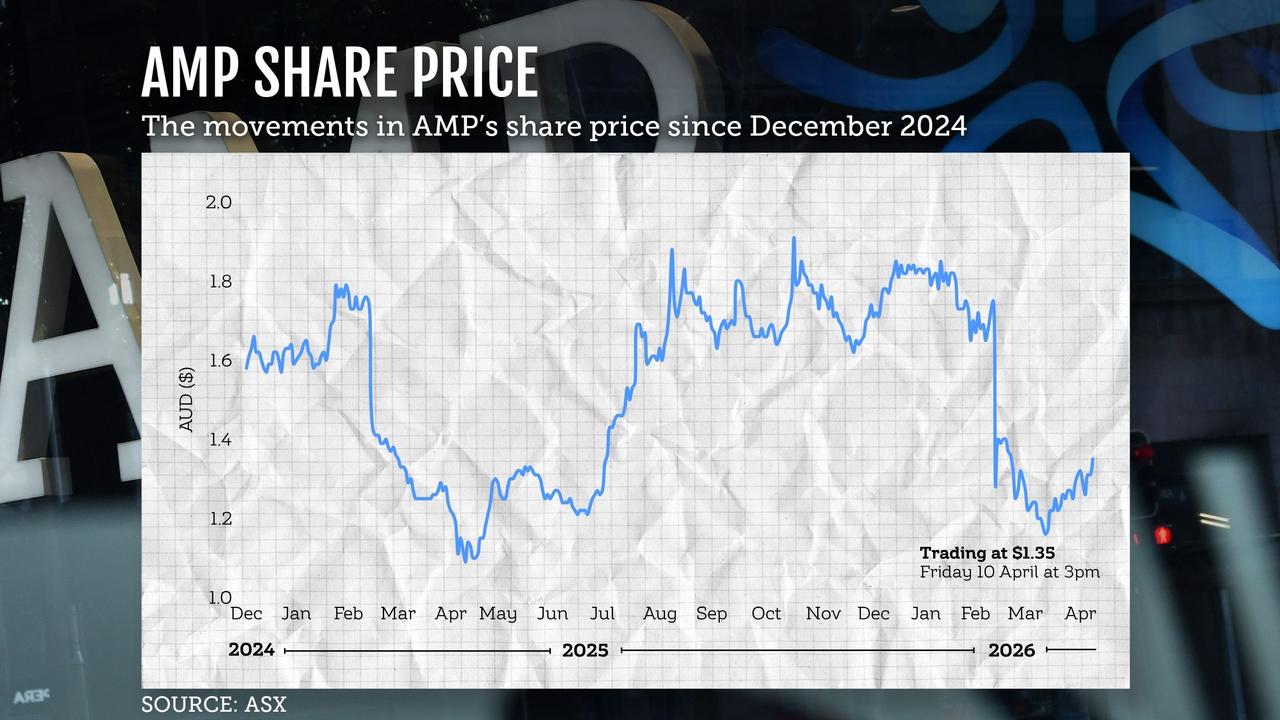

AMP leaders defend share price, tout AI future

Wealth management giant AMP has defended a post-earnings share price tumble, instead asking investors to look to its future.

Asked about the more than 25 per cent share price drubbing in February when it reported an 11 per cent fall in full-year profit, chair Mike Hirst said it had been a particularly volatile reporting season.

“If you have a look at CSL and other firms … Temple and Webster and others, you didn’t have to do much wrong to have an outsized reaction,” Mr Hirst told shareholders at AMP’s annual meeting in Sydney on Friday.

“Some people felt that the outlook wasn’t as positive as it could have been, although I note that all of the analysts who cover us currently have a share price of around $1.80 on the stock.”

AMP shares rose 2.3 per cent to $1.34 following the meeting, during which new chief executive Blair Vernon outlined his key priorities: organic growth, capital discipline and the adoption of artificial intelligence.

“There is simply no sideline position to take in this disruptive moment,” AMP’s former chief financial officer told shareholders.

“Most of our people are using AI regularly, with 84 per cent using our core AI tools on a weekly basis, so our focus right now is on enhancing the productivity gains with specific training and support for our people.”

AMP has been deploying the technology in contact centres for transcription and quality checking, to automate corporate functions and for note-taking in its super and pension wrap platform, North.

“This is just the start, and we’ll continue to leverage our deep knowledge and experience in retirement, along with the new technology to create seamless experiences and intuitive tools for advisors and our members,” Mr Vernon said.

Continued innovation in North, which assists advisors to manage client portfolios and superannuation, helped draw 120 advisors to the platform in the previous year, AMP’s chair said.

“North continues to gain momentum with new-to-platform and existing financial advisors, which is translating into industry recognition and improving net cash flows in our superannuation and investments business,” Mr Hirst said.

“We delivered strong investment performance with the majority of members receiving top quartile returns.”

Mr Hirst conceded the medium-term outlook for broader financial markets had been clouded by the energy price shock and subsequent inflation fears sparked by the Middle East conflict.

“It’s the volatility, I think, that’s the key impact, and I think it’s important that people try and see their way through that volatility by riding out the storm,” he said.

“Who knows how long it’s going to last? Hopefully it doesn’t go for too much longer …. but if I really knew the answer to that, I’d be extremely wealthy.”

Shareholders also raised concerns about the group’s retail banking offering and its AMP Bank Go app, following on from previous analysts’ questions about why AMP needed to offer banking services.

“The platform we’ve picked up for Bank Go is a proven platform from the UK, which is also now operating in other countries overseas,” Mr Hirst said.

The fall in AMP’s 2025 bottom-line net profit to $133 million was the latest in a string of declines since 2022, when it made a profit of $387 million.

Maila delays move on Qld, while Solomons count cost

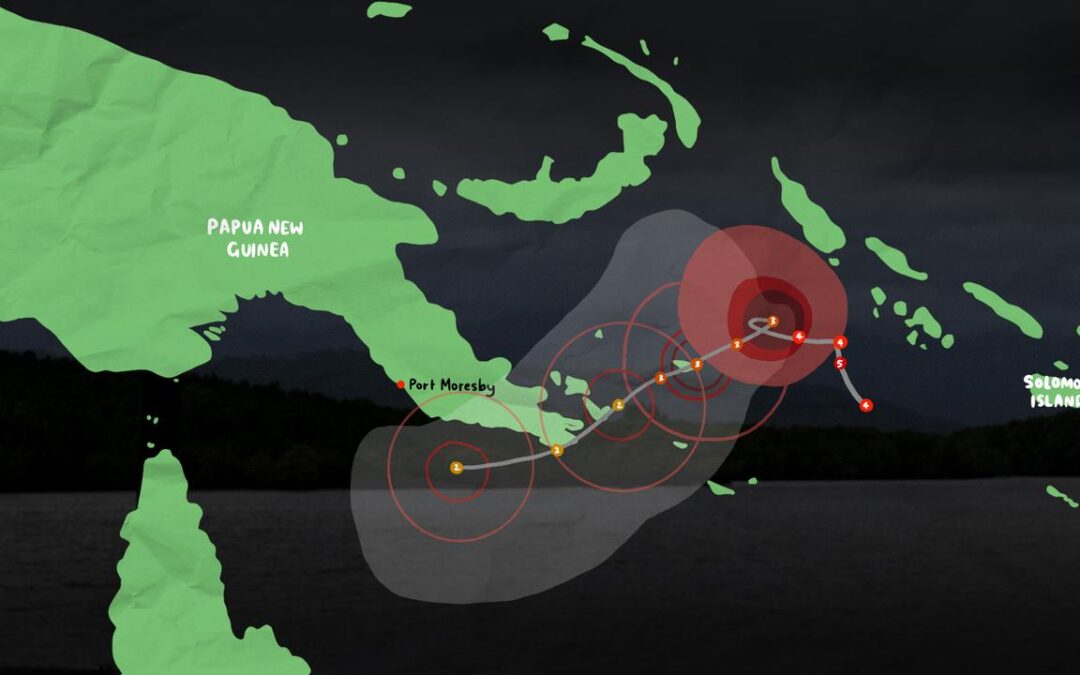

Tropical cyclone Maila has weakened again before a likely approach to Queensland, while Papua New Guinea is next in the firing line and the Solomon Islands is picking up the pieces.

Communities have been evacuated in remote parts of the Solomon Islands, with fears that many are without essentials.

The slow-moving storm – the strongest ever this far north in the Solomon Sea – has been battering islands for several days.

“These are very far flung places,” Save The Children country director Tory Clawson told AAP.

“There have been no boats or flights in and out for four days, so there’s a significant concern about food and water supplies.”

The most destructive winds have been at sea, with the eye nestled between the two Melanesian nations.

Outlying islands have been hit hard: there are reports of three people missing at sea, food shortages, and destruction of homes and crops in the Western, Choiseul, and Isabel Provinces.

Solomon Islands Prime Minister Jeremiah Manele gave a national address on Thursday, urging fishers to remain off the water and for communities to rally around the most affected.

The region’s biggest hospital, in Gizo, is in a state of emergency and only attending to emergency cases, according to the Solomon Star, with staff living in areas with damaged homes or at risk of landslides.

Storm surges have caused agricultural damage, while also contaminating drinking water.

Both are disastrous, especially given the high number of subsistence farmers, and the value of produce to trade at local markets.

Ms Clawson said establishing the full impacts and the scale of need would now be a priority.

“Many children and families have had to evacuate, often in the middle of the night,” she said.

“As recently as last night, storm surges at 3am in the morning, meant a community had to flee to higher ground.”

Mr Manele’s government has committed an A$1.76m package towards immediate humanitarian needs.

Maila was a category five system on Wednesday, with peak gusts up to 295kmph, but as of Friday afternoon, was classed as a category three, moving west towards PNG’s Milne Bay province.

Bureau of Meteorology tracking shows the storm will move across the region on Sunday as a category-two system, meaning the highest winds would be expected at 160kmph.

“From Sunday, Maila may track west southwest towards the Far North Queensland coast, possibly crossing Cape York Peninsula next week,” a BOM spokesman said.

PNG’s Woodlark Island, one of the biggest islands in the Solomon sea, is likely to be one of the hardest hit.

The cyclone’s path will determine its strength if and when it reaches Australia, with some models suggesting a downgrade to a less destructive tropical low.

“Another possible scenario is for Maila to weaken near or over southeast Papua New Guinea over the weekend and not cross the Queensland coast as a tropical cyclone,” the BOM said.