Aussie shares rebound on tentative ceasefire deal

Australia’s share market is on track to finish a volatile week where it began, after equities rebounded on reports that the US and Iran will extend a fragile ceasefire to finalise a lasting peace deal.

The S&P/ASX200 rose 80.8 points by midday on Friday, to be up 0.94 per cent, at 8,637.7, as the broader All Ordinaries gained 89.1 points, or 1.01 per cent, to 8,908.7.

“The US and Iran are reportedly on the cusp of a deal to extend the ceasefire for another 60 days, with the agreement said to include a toll-free re-opening of the Strait of Hormuz,” Capital.com senior market analyst Kyle Rodda said.

“The move in oil prices was negligible, suggesting a peace premium is all but priced-in into the market – setting up the markets for big disappointment if this purported deal proves to be another false dawn.”

Wall Street indices surged to fresh record highs overnight, buoyed by geopolitical developments and softer-than-expected US economic data, which kept hopes of Federal Reserve interest rate cuts alive.

“The markets are as bullish as they’ve been since the start of the war, with risk appetite amply whetted,” Mr Rodda said.

Brent crude tumbled to six-week lows overnight to trade at $US92.34, dragging on local energy oil and gas giants Woodside and Santos, which dipped one per cent and 0.6 per cent respectively.

Refinery operators Ampol and Viva sold off, along with coal miners, while uranium stocks rebounded from recent weakness.

Industrials advanced as Qantas and Virgin Australia soared more than two per cent each on the prospect of easing jet fuel prices, while Transurban, Brambles and Computershare also improved.

Mining stocks continue to see-saw on the whims of the US-Iran conflict, the basic materials sector bouncing 2.4 per cent on Friday morning and on track for a positive week.

Mega miners BHP, Rio Tinto and Fortescue each pushed higher, despite iron ore futures slipping to six-week lows on growing concerns of a supply glut and softer-than-expected steel demand from China.

The gold price firmed to $US4,535 ($A6,331) an ounce, boosting the commodity’s local sub-industry 4.7 per cent.

The heavyweight financials sector improved by 0.4 per cent, led by rebounds of similar magnitudes from ANZ and NAB.

Commonwealth Bank shares rose 0.2 per cent by lunchtime to $161.80, roughly 18 per cent from all-time highs but clear of 2026’s $146.98 low.

Real estate stocks surged 1.3 per cent and are on track for a positive week, while discretionary retail added 0.7 per cent.

The Australian dollar was buying 71.61 US cents, up from 71.22 US cents on Thursday at 5pm.

Oil eyes weekly drop on Hormuz deal hopes

World stocks stood at record highs on Friday and oil futures eyed the steepest weekly drop for nearly two months as traders waited for details on a potential deal to reopen the Strait of Hormuz and extend the US-Iran ceasefire.

Sources told Reuters that the US and Iran have reached an agreement to extend their ceasefire and lift restrictions on shipping, though US President Donald Trump has yet to approve it and Iranian state media said it had not been finalised.

Moves in the Asia morning were modest, with S&P 500 futures steady after the index notched another record closing high overnight. Brent crude futures fell about 50 cents a barrel to $US93.17 ($A130.36) for a weekly drop of more than 10 per cent.

The dollar headed for a small fall on the week, which tracks a retreat in US yields. Analysts aren’t sure, however, whether that can extend, since a US-Iran deal is unlikely to quickly unwind the inflation impulse unleashed by soaring fuel prices.

“The market’s already taking the view that a deal’s going to be done and the strait is going to be open,” said Jason Wong, senior market strategist at BNZ in Wellington.

“The main point is it removes a tail risk of a really, really bad outcome. I don’t think it’s a green light to take oil down $US20 ($A28), or Treasuries down 20 points.”

MSCI’s index of world stocks edged up to a record high, with AI-euphoria lifting chipmaker shares around the world and pushing benchmarks in Tokyo and Seoul up around 2.0 per cent on Friday morning and toward weekly rises.

Dell was also riding the wave, with shares soaring 39 per cent after hours when it lifted revenue and profit expectations as data-centre demand drives sales of its AI-optimised servers.

“The question now is whether this can continue. We believe we’re still in the middle innings of a longer AI-driven investment cycle,” said Damian McIntyre, head of multi-asset solutions at asset manager Federated Hermes.

“We have revised our S&P 500 target to 8,000 this year and 9,000 next year.”

The S&P 500 closed on Thursday at a record high of 7,563.63.

In fixed income, US Treasury yields were steady in the Asia day, with the 10-year yield at 4.45 per cent for a weekly drop of about 14 basis points. Global bond yields are also lower on the week.

Preliminary inflation figures are due across Europe later in the day, along with Canadian GDP. Overnight data showed US personal consumption spending, income, home sales and GDP on the soft side of expectations, and inflation running hot but a little bit under forecasts.

Annual core inflation in Tokyo stayed below Japan’s 2.0 per cent target for a fourth straight month in May, data showed on Friday, but a rebound in national factory activity suggested resilience and supported the case for a June rate hike.

In currency markets the yen has been under pressure and in focus after falling back to levels that prompted reported Japanese intervention late in April and earlier in May.

At 159.26 to the dollar it was trading a fraction stronger than the line-in-the-sand around 160 that authorities have been defending.

Japan’s finance ministry is scheduled to publish the amount of dollar selling it conducted, with estimates it totalled around 8.6 trillion yen ($A76 billion), Nomura said.

The euro was firm at $US1.1655 ($A1.6307). The New Zealand dollar has been a major mover this week, up 1.8 per cent on the greenback, after the Reserve Bank of New Zealand held rates steady on Wednesday but delivered a more-hawkish-than-expected outlook.

‘Vested interests’ protest against housing tax changes

Rival forecasts showing a dire outcome for renters from the government’s tax changes are being dismissed by Labor as the work of “vested interests”.

Health Minister Mark Butler said it was hardly surprising the real estate lobby would defend the status quo after property industry groups released modelling claiming the impact of the tax package would be worse for rent prices and housing supply than Treasury forecasts.

The modelling, conducted by economic consultancies Qaive and Tulipwood and released jointly by the Real Estate Institute, Master Builders, and the Property Council, showed the budget would cause 8700 fewer new homes to be built over the next four years.

Rents would be $9 a week higher, Australia’s economy would be $864 million smaller and there would be 3800 fewer construction jobs than would otherwise be the case, the analysis found.

The modelling took into account changes to negative gearing and the capital gains tax discount, as well as $2 billion to fund enabling infrastructure and boost construction productivity, included in the budget.

According to opposition housing spokesman Andrew Bragg, the modelling confirmed suppressing housing supply in a housing crisis was a deliberate design feature of Labor’s budget.

The outcomes were significantly more pessimistic than Treasury’s modelling, which found rents would only increase by $2 a week and housing supply would be 30,000 higher over a decade.

Much of the variance can be explained by different assumptions about the enabling infrastructure fund, which the property industry’s modelling found would only result in 5300 new homes over four years compared to Treasury’s expectation of 26,000 new homes.

Mr Butler said the government would back the modelling of Treasury officials, who were employed by the public to work in the public interest and “not in the interest of vested interests”.

“I’m not sure people will be particularly shocked that the real estate industry, for example, is very happy with the status quo,” he told Seven’s Sunrise program on Friday.

“What a surprise that they’ve got some modelling that indicates the government should do absolutely nothing.”

Mr Butler cited forecasts from independent think tank the Grattan Institute, which estimated the changes would result in an increase in median rents of just $1 per week.

Negative gearing arrangements would be grandfathered for existing investors, which meant there was no basis for them to increase rents, Mr Butler said.

In a post-budget address on Thursday, Treasury secretary Jenny Wilkinson said the reforms would reverse a decade of declines in home-ownership rates.

“Over the next decade, owner‑occupiers are projected to own around 75,000 more homes than they would have otherwise,” she told the Australian Business Economists lunch in Sydney.

“This reallocation of housing stock, which improves opportunities for first-home buyers, is a result of reduced investor demand in the existing housing market.”

Online spaces, social media speeding up radicalisation

Young Australians are being moved to violent extremism in a matter of days as the speed and scale of radicalisation accelerate.

For years, terrorists and extremists have used the internet to target young people and convince them to plan and carry out violent acts.

But the recent use of social media, gaming platforms, online forums, the dark web and private group chats has allowed bad actors to more quickly and effectively radicalise people, the Australian Federal Police warns.

“Where it used to take months or years to radicalise a person, in some cases, it’s happening in days,” AFP Commissioner Krissy Barrett told senate estimates on Thursday.

“We see the speed and scale of radicalisation becoming one of our most significant challenges, especially when it comes to young people.”

The problem is not exclusive to Australia.

Security agencies internationally are battling growing radicalisation and the commissioner has said the issue will take the spotlight when she attends a meeting with counterparts from fellow Five Eyes nations – the UK, US, Canada and New Zealand – in June.

The countries are exploring the possibility of allying with tech companies to use artificial intelligence and other emerging technologies to combat radicalisation, particularly targeting young people.

Of the 32 people charged with violent extremism material offences by Australia’s joint counter-terrorism team, 19 were no older than 17, and some were as young as 13.

The federal government has pledged $74 million over the next two years to establish a national Counter Terrorism Online Centre to address the issue.

Ms Barrett said it would allow police to identify and disrupt radicalisation earlier and protect vulnerable young people.

It will provide an early warning system for Australia’s joint counter-terrorism teams about hate groups and others who might be using the internet to incite violence.

Prime Minister Anthony Albanese also said his government would engage “in good faith” with states’ requests for more federal funding for deradicalisation.

“Every state and territory wants more money for everything,” Mr Albanese said on ABC’s Afternoon Briefing on Thursday.

“I won’t discuss issues related to national security on your program, frankly.”

NSW, which is managing the processing of several women returned from Syrian detention camps, made a specific request for money to support health checks and reintegration, federal government officials confirmed at a Senate inquiry on Wednesday.

The Albanese government is yet to issue a response to the request.

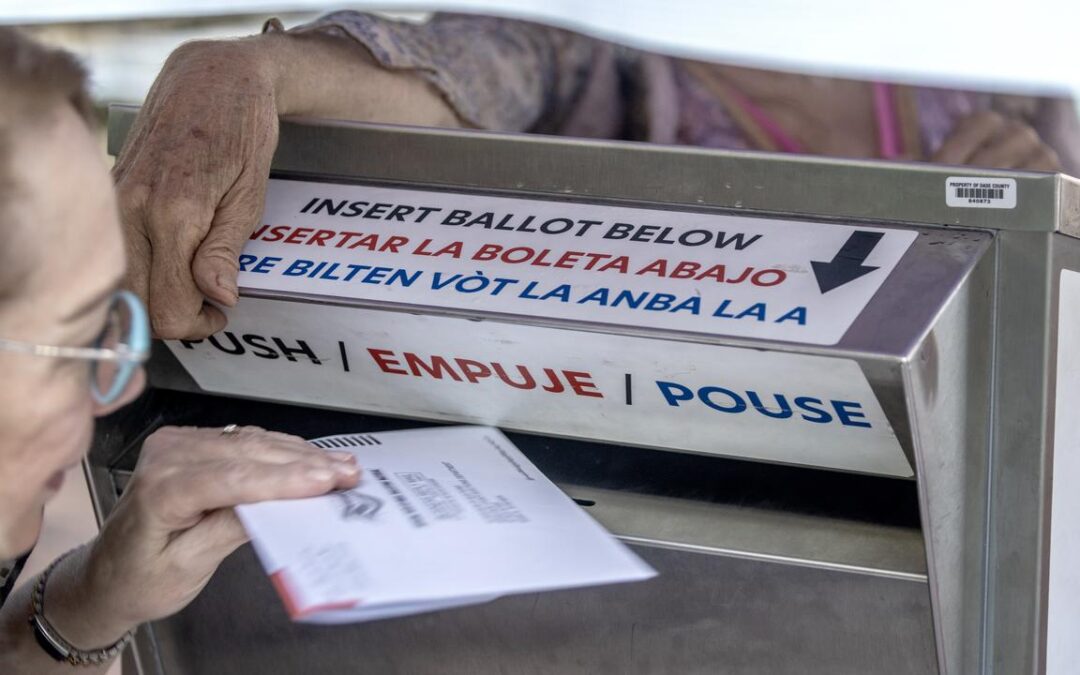

Judge allows Trump to implement mail-in voting order

A US judge has declined to block President Donald Trump’s executive order tightening rules on mail-in voting in a loss for the Democratic Party, whose lawyers argued it could disenfranchise millions of voters.

The decision on Thursday comes as Trump’s Republicans are locked in a tight battle to keep control of both houses of the US Congress in the November midterm elections.

Trump has for years pushed the false claim that his 2020 election defeat was the result of widespread voter fraud and has criticised voting by mail.

The executive order signed by Trump on March 31 directed his administration to compile a list of confirmed US citizens eligible to vote in each state and to use federal data to help state election officials verify who is eligible to vote.

It also required the US Postal Service to only deliver ballots to voters on each state’s approved mail-in ballot list, and required states to preserve election-related records for five years.

In rejecting a request by plaintiffs including Senate Minority Leader Chuck Schumer of New York that he issue a preliminary injunction blocking the measure, Washington-based US District Judge Carl Nichols wrote that the Democrats had brought the case too early because the government had not yet produced any flawed citizenship lists and the Postal Service had not yet implemented any new rules.

“Given that the executive order does not command plaintiffs to do anything, and that no agency has yet acted pursuant to the Order in a way that could harm plaintiffs, they have not suffered any harm at present,” wrote Nichols, who was appointed by Trump during his first term.

The judge said the Democrats could ask for an injunction again after federal agencies took steps to implement the executive order.

Democrats had argued the order infringed on individual states’ rights to regulate elections under the US Constitution.

A coalition of Democratic states brought a similar lawsuit challenging the executive order in federal court in Boston.

US District Judge Indira Talwani, an appointee of Democratic former President Barack Obama, is due to hear arguments in that case on June 2.

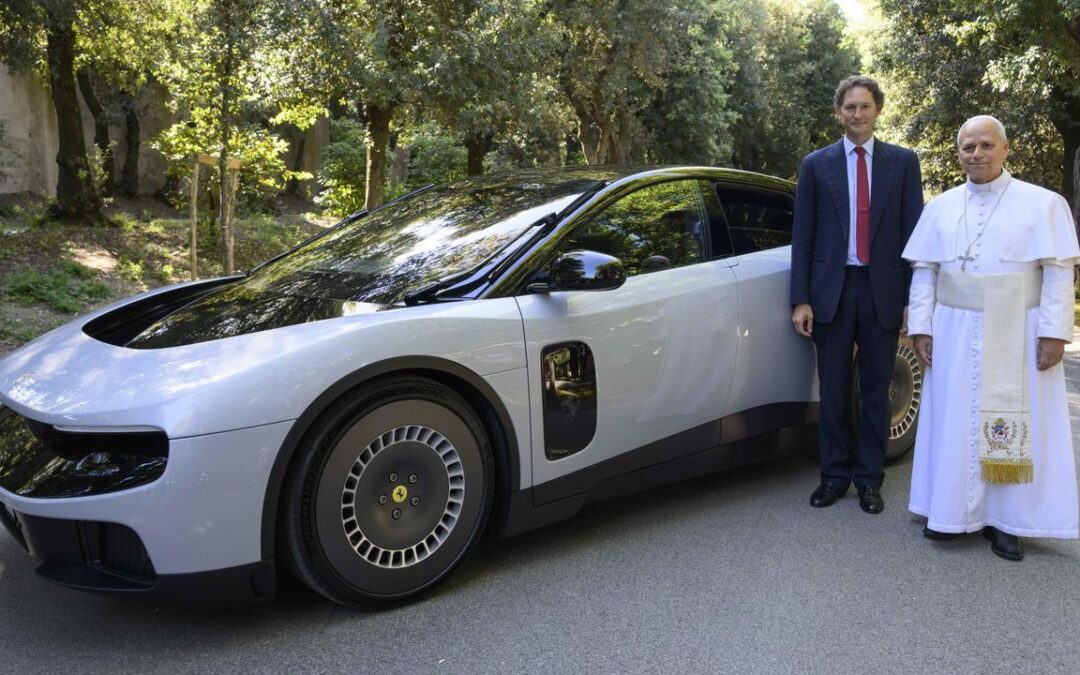

Ferrari aims to prove doubters wrong after EV debut

If Ferrari wanted to grab the world’s attention with the Luce, its first all-electric car, mission accomplished – even if much of the reaction has been shock and outrage.

The new model is a four-door, five-seat family car that looks nothing like the Italian marque’s usual fare of low-slung, petrol-powered sports cars.

It was unveiled at a gala event in Rome late on Monday, then shown the next day to Italian President Sergio Mattarella and Pope Leo, a well-known car enthusiast who appeared happy to take the driver’s seat.

But the styling, largely the work of auto industry outsiders Jony Ive and Marc Newson and their collective LoveFrom, has left many fans and commentators baffled. Ive is best known as the designer of Apple’s iPhones and MacBooks.

Social media is awash with unflattering memes, comparing the Luce variously to a vacuum cleaner, a rubber clog or the much-maligned Fiat Multipla, a 1990s people carrier often cited among the world’s ugliest cars.

Italian Deputy Prime Minister Matteo Salvini publicly wondered what founder Enzo Ferrari, who died in 1988, would make of it.

Former Ferrari chief executive Luca Cordero di Montezemolo said the car should be stripped of the prancing horse logo.

Investors flinched, too. Milan-listed Ferrari shares fell 8.4 per centon Tuesday, with one investor telling Reuters the stock was “being penalised for an aesthetic disappointment”.

Felipe Munoz of Car Industry Analysis said Ferrari likely anticipated the uproar, given the deliberate break with tradition, and noted negative publicity was still publicity.

“From a communication standpoint, they have managed to get the world talking about the electric Ferrari,” he said.

“As far as awareness goes, they have made it, because there is no other topic at the moment.”

Munoz described the Luce as a “statement product” – unlikely to be a big seller but key to showcasing technology and repositioning Ferrari in the electric age.

A company source noted earlier Ferrari curveballs – the all-wheel-drive FF in 2011 and the Purosangue SUV in 2022 – also drew scepticism before going on to sell well.

AFP defends Roberts-Smith arrest as media leak probed

The Australian Federal Police has defended its prosecution of the nation’s most decorated living soldier as a media leak about his arrest comes under scrutiny.

Ben Roberts-Smith was charged with murdering or ordering the murders of five unarmed detainees while deployed in Afghanistan between 2009 and 2012, after he was sensationally arrested on the tarmac of Sydney Airport in April.

Following a flight from Brisbane, the Victoria Cross recipient was met by one media outlet’s camera crew as AFP officers walked him off the plane.

No other media organisations were made aware of the arrest ahead of time.

The department responsible for investigating war crimes has asked the federal anti-corruption commission to probe the leak, and on Thursday, AFP Commissioner Krissy Barrett backed the decision.

“I am not just disappointed the media outlet was there, but I am determined to find out how they knew of the arrest,” she told Senate estimates.

“This could be an unauthorised disclosure and in my view anyone who disclosed that information should face consequences.

“I have no evidence to suggest the AFP provided information to the media about the date or details of the arrest.”

Other details of his arrest have been questioned by Liberal senator Michaelia Cash and One Nation senator Malcolm Roberts, who asked why he was arrested in front of his teenage daughters and why the AFP shared its official footage – which blurred Roberts-Smith’s face – after the arrest.

Acknowledging the “legitimate interest” in the issue, Ms Barrett offered a comprehensive statement.

A joint war crimes investigation into members of the Australian Defence Force deployed to Afghanistan was first launched in December 2021.

The Sensitive Investigations Oversight Board on March 31 proposed charging Roberts-Smith and on April 1 it received consent from Attorney-General Michelle Rowland, which led to the 47-year-old’s arrest on April 7.

He was taken into custody at Sydney Airport due to operational reasons, the commissioner said.

The sterile environment at an airport, where people are screened and the area is contained, makes it safer for members of the public and for AFP officers to take action.

There were reports Roberts-Smith had offered to present himself to police, but this was “unviable” due in part to the seriousness of his charges, Ms Barrett said.

The AFP also makes footage available to the media to officially document an arrest and offer a source of truth in an era of misinformation.

“We take an oath that we will faithfully and diligently carry out our duties without fear or favour, without affection or ill will,” Ms Barrett said.

“The Australian public can know the AFP will determine cases on the evidence in front of us, and not because of name, fame, or background of any individual, and that is the right thing to do.”

The former SAS soldier has promised to use the upcoming trial to clear his name.

Data centres drive record $6 billion investment boom

The Iran war appears to be having little impact on Australia’s data centre boom, but households are starting to feel the pinch.

Private capital expenditure jumped 6.5 per cent in the first three months of 2026, smashing consensus expectations of a 1.2 per cent rise, the Australian Bureau of Statistics reported on Thursday.

That was driven by a near tripling in spending on information media and telecommunications equipment to a record $6 billion in the quarter.

It followed a similar spike in the three months to September 2025, ABS head of business statistics Tom Lay said.

“The lift in investment was the result of investment in data centre equipment, specifically server racks and processing equipment, significantly boosting overall investment figures,” Mr Lay said.

Billions more were being poured into productive investment, which was good news for Australia’s economy, Treasurer Jim Chalmers said.

“These kinds of infrastructure projects are a priority for our government, and clearly, they’re a priority for the private sector as well,” he said in a statement.

Overall, the figures showed private business investment was holding up in Australia, which is good news for growth prospects, AMP deputy chief economist Diana Mousina said.

“But some broadening out across the sectors would be helpful, particularly as manufacturing has continued to shrink and as mining is flat-lining,” she said.

Beyond data centres, Australia’s investment outlook looked subdued amid higher interest rates and offshore uncertainty, Commonwealth Bank head of Australian economics Belinda Allen said.

While the data centre boom continued to prop up business investment, households were beginning to wobble as a result of the Middle East conflict.

Household spending fell 1.1 per cent in April after a 1.6 per cent rise the month before, according to ABS data.

It was the steepest monthly decline since October 2023, but was largely driven by cheaper travel costs as a result of the government’s fuel excise cut and free public transport in Victoria and Tasmania.

Experimental data produced by the bureau suggested that the volume of fuel spending actually increased by two per cent in April.

Even excluding travel spending, the figures showed weakness creeping into the economy.

Discretionary spending fell 0.8 per cent, driven by reduced spending on clothes, services and air travel – although part of that was due to refunds from cancelled flights.

The weakness in spending is consistent with other soft economic indicators lately, including fragile consumer confidence, low auction clearance rates and slightly better than expected inflation data for April, ANZ head of Australian economics Adam Boyton said.

“The latter suggests that firms might be struggling to pass price and cost increases through to consumers,” he said.

‘Huge mistake’: how Howard spurred Boomer investors

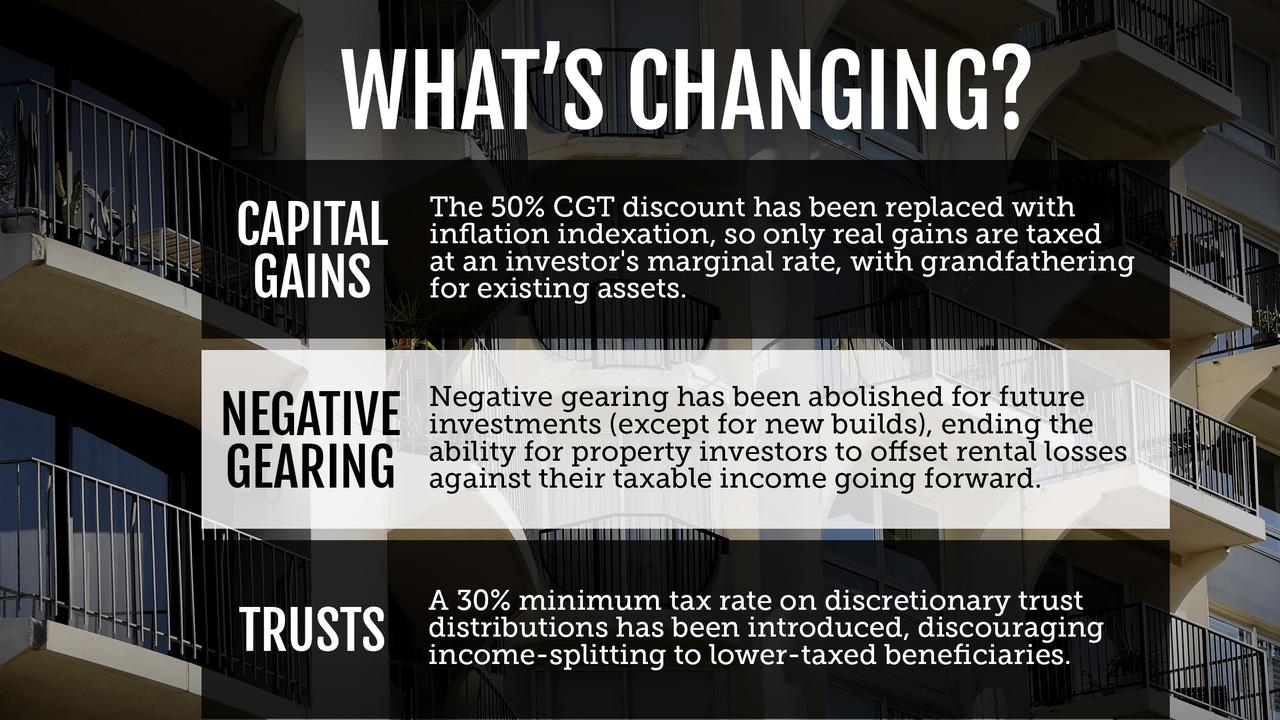

A controversial tax reform package will correct a “huge mistake” that locked a generation of people out of home ownership, Labor says.

Reserve Bank research has found the proportion of Baby Boomer property investors has surged since the capital gains discount was introduced.

As changes to negative gearing and the capital gains tax were introduced to parliament on Thursday, Housing Minister Clare O’Neil told the National Press Club the Howard government created a “perfect storm” in Australia’s housing market.

By introducing the 50 per cent capital gains discount in 1999, investors piled into the market when declining building productivity was already weakening supply.

“The result? You can find it in any economics textbook in the world,” Ms O’Neil said.

“House prices sharply detached from incomes. Rents surged. And homelessness rose in a country where we should never accept this as inevitable.”

A generation had been locked out of home ownership, she said, accusing the coalition of trying to defend a broken status quo.

Research by Reserve Bank senior analyst Alexandra Michielsen showed 12 per cent of housing investors were older than 60 in 2000, the year after the Howard-era reform.

In 2023, that proportion had surged to 28 per cent.

The share of investors younger than 30 fell from nine per cent to four per cent in the same period.

Opposition housing spokesman Andrew Bragg called the tax changes “crazy policy”, saying Treasury’s analysis found it would reduce housing supply by 35,000 homes.

But economists at Westpac found the tax changes might eventually drive an annual lift in dwelling construction of 15,000 to 30,000 per year, as a result of a carve-out for new builds directing investor activity away from established housing.

The government argues other policies encouraging supply, including $2 billion for so-called last-mile infrastructure and a $40 million package to encourage modular construction, would result in a net increase in homes built.

The funding would support a trial of modular, pre-made building components which could speed up construction times while driving down costs, Ms O’Neil said.

“It means building smarter and faster, using standardised components like bathroom pods, wall panels and facades,” she said.

The funding announced on Thursday will go towards a “kit of parts” – a system of home components that can be built off-site and assembled similarly to a supersized IKEA flat-pack.

In Sweden, about 80 per cent of detached homes are built using prefabricated parts, compared to just five per cent in Australia.

The system is the brainchild of Building 4.0 CRC – an industry-led research group partly funded by the federal government – and is open-source, meaning businesses across the country can participate without relying on a single proprietary company.

The federal funding would help the states and territories with pilot projects, design work, technical advice, training and supply chain development, Ms O’Neil said.

National Shelter, a housing advocacy non-profit organisation, said the funding would help tackle one of the most stubborn barriers to delivering modern construction methods at scale.

“There is simply no pathway to meeting our future housing needs without the adoption of new and innovative housing,” the body’s chief executive Jackson Hills said.

The government also wants more social housing to be made from prefabricated parts, as this would create a pipeline of work for the so-far nascent industry in Australia.

Building 4.0 CRC chief executive Mathew Aitchison said his organisation would work with governments and industry to help roll out the kit of parts.

While he supported the government encouraging prefabricated and modular construction, the overstuffed National Construction Code was making it too difficult to build cheap homes, Senator Bragg said.

Shares drop and oil surges as US, Iran trade strikes

Australian shares have had their worst day since mid-March after a re-escalation in the US-Iran conflict dimmed peace deal hopes and boosted oil prices.

The S&P/ASX200 fell 124.8 points on Thursday, down 1.43 per cent, to 8,592.9, as the broader All Ordinaries dropped 125.6 points, or 1.4 per cent, to 8,819.6.

Gold fell to a two-month low and oil surged more than three per cent after Iran’s Revolutionary Guard claimed to have targeted a US military base and Kuwait reported intercepting hostile missiles and drones.

The local exchange’s two biggest sectors took some of the heftiest losses on Thursday, with basic materials down 2.4 per cent and financials slumping 1.6 per cent by the close.

The Australian dollar is buying 71.17 US cents, down from 71.46 US cents on Wednesday at 5pm.