Sixty one. That’s the additional number of days women currently have to work in a financial year to earn as much as their male counterparts. And when it comes to superannuation, the gender gap gets worse, writes Harry Chemay.

Few policies touch the lives of Australians so directly as superannuation. For some, it has created opportunities for tax-efficient wealth in their golden years. But for a system that now exceeds $3.3 trillion in total value, the outcomes it produces are far from equitable, and highly gendered.

Decades after the passage of the Sex Discrimination Act in 1984 and the more recent Workplace Gender Equality Act of 2012, the gap remains. According to the Workplace Gender Equality Agency (WGEA), there’s now a 14.2% ‘Gender Pay Gap’ between the average earnings of women and men in the workforce.

Men and women performing the same work are, on the face of it, required by law to be paid the same amount. But pay equity, or an absence thereof, is only a small part of the gender pay gap.

The gap instead speaks to a range of issues that see females enter the workforce in near pay parity with males, but with a gradual divergence thereafter in job opportunities, career trajectories and lifetime income earning capacity.

All of which compound over time into poorer outcomes later in life, particularly when it comes to financial security in retirement. Superannuation simply isn’t a level playing field between the sexes.

Super is great for males, not so much for females

Superannuation relies on the benefit of compounding interest to add to the impact of contributions. That compounding effect works best off a solid base of contributions made as early as possible.

This is the first disadvantage women face. WGEA stats show that despite having superior educational outcomes to males when entering the workforce (of all women aged 25 – 29, 48.3% have a bachelor degree or higher compared to 36.1% of similar-aged males), the median undergraduate starting salary for females is 2.5% less than for males.

From there, things only get worse for females, particularly in the private sector, where the gender pay gap currently runs at 20.1% for full-time annualised total remuneration.

Women are also more heavily represented in part-time work. While females comprise 47% of all employed persons, they make up 68% of all part-time employees.

But even women on a high trajectory career path aren’t on a level playing field, with females holding fewer than 33% of key management positions, and only 18% of CEO roles.

Even absent career breaks, the higher lifetime incomes experienced by males translate into higher employer Superannuation Guarantee contributions, giving men a leg-up in the compounding stakes, and an unassailable lead, on average, in the race for retirement security.

In tying the guarantee to average weekly earnings, of which full-time females currently derive $261.50 less on average, gender inequity is built into the architecture of the modern superannuation system.

Emergency piggy-bank: superannuation’s Achilles heel exposed by virus

Addressing the super gender imbalance

Last year’s Retirement Income Review (RIR) looked at the issue of the adequacy, equity and sustainability of the retirement income system in a mammoth 600-plus page report commissioned by the Government.

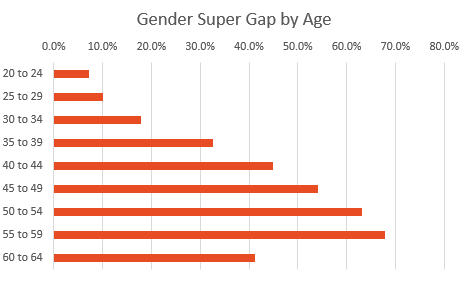

It stated that the 2017-18 median balance for super for those aged 60 – 64 (the age range at which most Australians retire) to be $163,985 for men and $128,507 for women.

But when looking at different age groups the gaps blow out to over 60% in the all important ‘peak earning’ years before narrowing slightly at retirement age.

The RIR also found that career breaks for child rearing is a significant impediment to retirement equity.

Women represent 94% of all carer’s leave. One study shows a woman with a child aged two or younger in 2001 experienced an average 77.5% reduction in earnings over the subsequent 15 years, compared to those without children. Men with young children faced no similar penalty.

The government’s policy is to mitigate this through the Parental Pay Leave payment. This costs the Budget some $2.2 billion per year, made at the minimum wage to eligible persons for up to 18 weeks. But it excludes superannuation. An easy fix at the cost of a relatively paltry $220 million or so per year.

Late-life relationship breakdowns

The other major gender factor in retirement security revolves around relationship status.

According to the RIR, some 19% of women and 15% of men aged 60 – 64 were divorced and single in 2016, up from 6.7% and 6.3% in 1991 respectively.

The report found that women were generally under-enforcing their rights to the super assets of their ex-partners in settlement proceedings, ending up with less super than what they could have.

![Chart-2-RIR-Retirement-Income-Breakdown[1]](https://www.michaelwest.com.au/wp-content/uploads/2021/09/Chart-2-RIR-Retirement-Income-Breakdown1.png)

This is wholly consistent with single females, especially those on lower incomes, having less super from which to meet retirement living expenses than single males.

A man is not a retirement plan, housing security is

The face of tomorrow’s struggling retiree is likely to be that of a single female renter.

A study by the Australian Human Rights Commission found that women over 55 are the fastest growing homeless group in the country. This strongly suggests the difference between a retirement of relative security versus one of poverty is based on home ownership status at retirement.

Unencumbered homeownership produces a retirement ‘income’ of sorts, being the amount not spent on rent. This equates to around $20,000 per year, the national average rent for a house.

Avoid the rent payments and receive a full single age pension, together with superannuation and a little private savings, and retirement might still not be champers and foie gras, but neither will it be precarious.

Academic research clearly shows that the edges of home ownership are becoming more porous. Women who exit home ownership later in life are finding it increasingly difficult to re-enter the market, and if they do, to retire without significant debt outstanding.

Neither approaching retirement as a single renter, nor being highly encumbered with mortgage debt, is desirable if retirement security is the goal.

The Commonwealth Rent Assistance needs to be raised to help the growing number of retiree renters, particularly single females for whom the current maximum rate is a paltry $140.80 per fortnight.

Today’s crumbling housing affordability also presents a real and present danger to the future financial security of all Australians, irrespective of the generation to which they belong.

Snakes and Ladders: stimulus schemes and debt skew economy as property prices rocket

That, unfortunately, appears to be a policy problem being deferred into perpetuity. Upsetting constituents sitting on mountains of owner-occupier and investment property housing wealth is not a good election strategy.

Harry Chemay has more than two decades of experience across both wealth management and institutional asset consulting. An active participant within the wealth and superannuation space, Harry is a regular contributor to investment websites in Australia and overseas, writing on investing and financial planning.