On negative gearing and CGT. Jim Chalmers’ aim is to ease intergenerational inequality while lifting Australia’s woeful productivity. Harry Chemay reports on the Budget.

Before I dive into this Budget follow-up piece, a confession. Some of what I’m about to explain can be attributed to a lifelong interest in economics, an interest that goes back to Year 11, then continued through university into my professional life.

Here’s what I learned. The total production of an economy is essentially equivalent to its income. I’ll spare you the GDP formula that all economics students would have had seared into memory early on, but the key thing is this: investment is not the same as savings.

Firms invest and households save. And yes, that includes shares in listed companies and holdings in residential investment properties. If it isn’t increasing the productive capacity of the economy (such as in plant, equipment, training and R&D), it’s savings not investments.

Sure some of these savings structures (such as the land on which a residential investment property sits) may increase in value over time but that isn’t, in and of itself, adding to Australia’s ability to create goods, services and intellectual property, produce them, trade, export and so generate income, the sum total of which (excluding imports) is our national GDP.

There are countries that understand this, like some dynamic economies to our north, and there are those that struggle with it.

Unfortunately, Australia is in the latter camp.

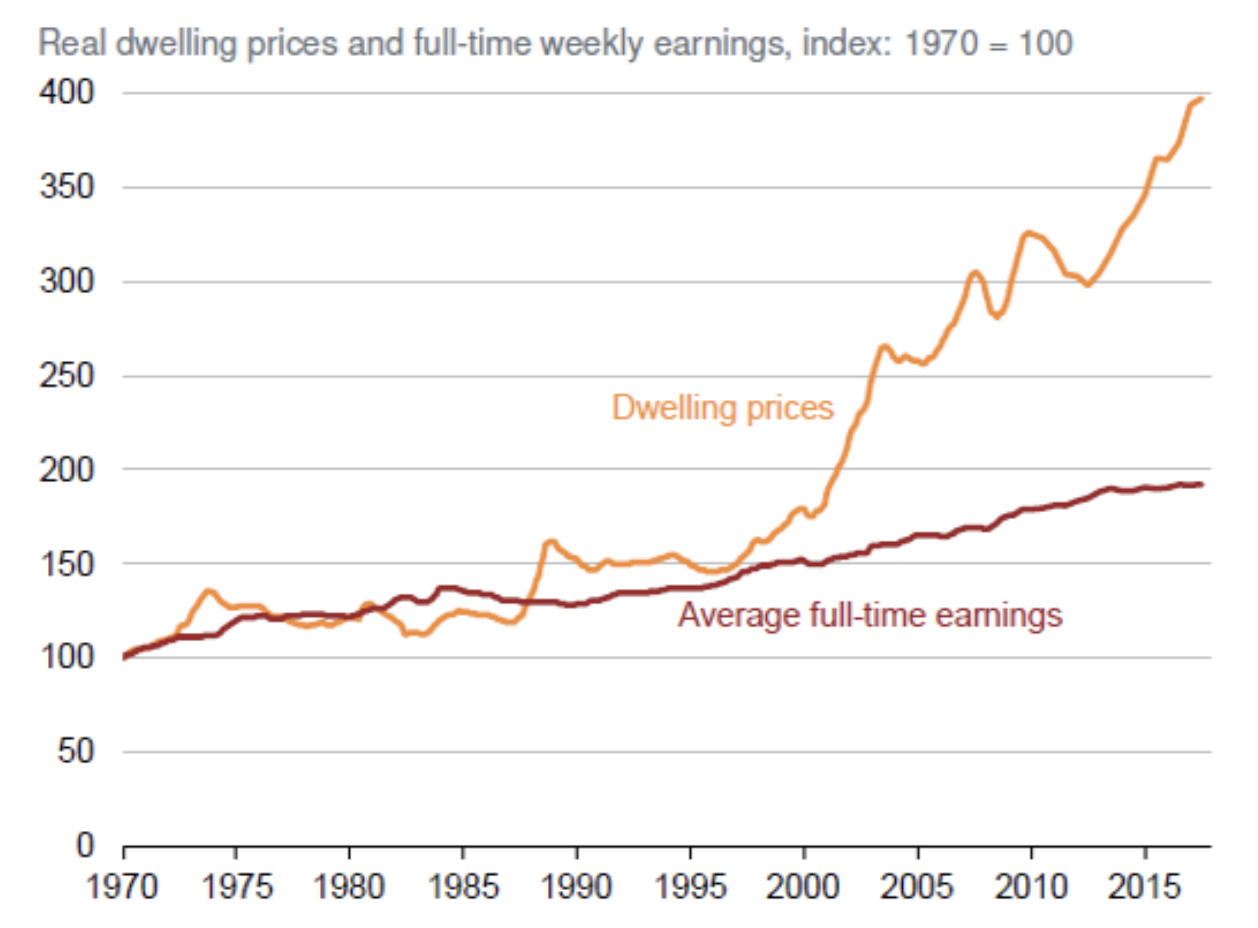

Housing obsession fails productivity

Which is why, at $12 trillion, we have a housing market almost four times as large as the market value of all companies listed on the ASX. That in turn has cratered housing affordability while strangling economic productivity (income the economy can generate for each work hour), leading Paul Schroder, CEO of the largest super fund in Australia, last year to observe that:

“[Housing] is the crisis that is facing Australia. All we’ve done is pour all this money into houses, which has deprived the economy of heaps of productive capital. We’ve got all this money in our domestic houses and we’re not backing business, we’re not creating new things, we’re not driving productivity”.

Noting that economic productivity drives long-term household income growth, the below chart from the Grattan Institute would seem to validate Schroder’s comments.

This disconnect is what this latest Budget aims to address, through cutting business red tape while reigning in house price speculation via negative gearing.

Housing affordability. The crisis the major parties are too scared to fix

Tightening negative gearing and CGT concessions

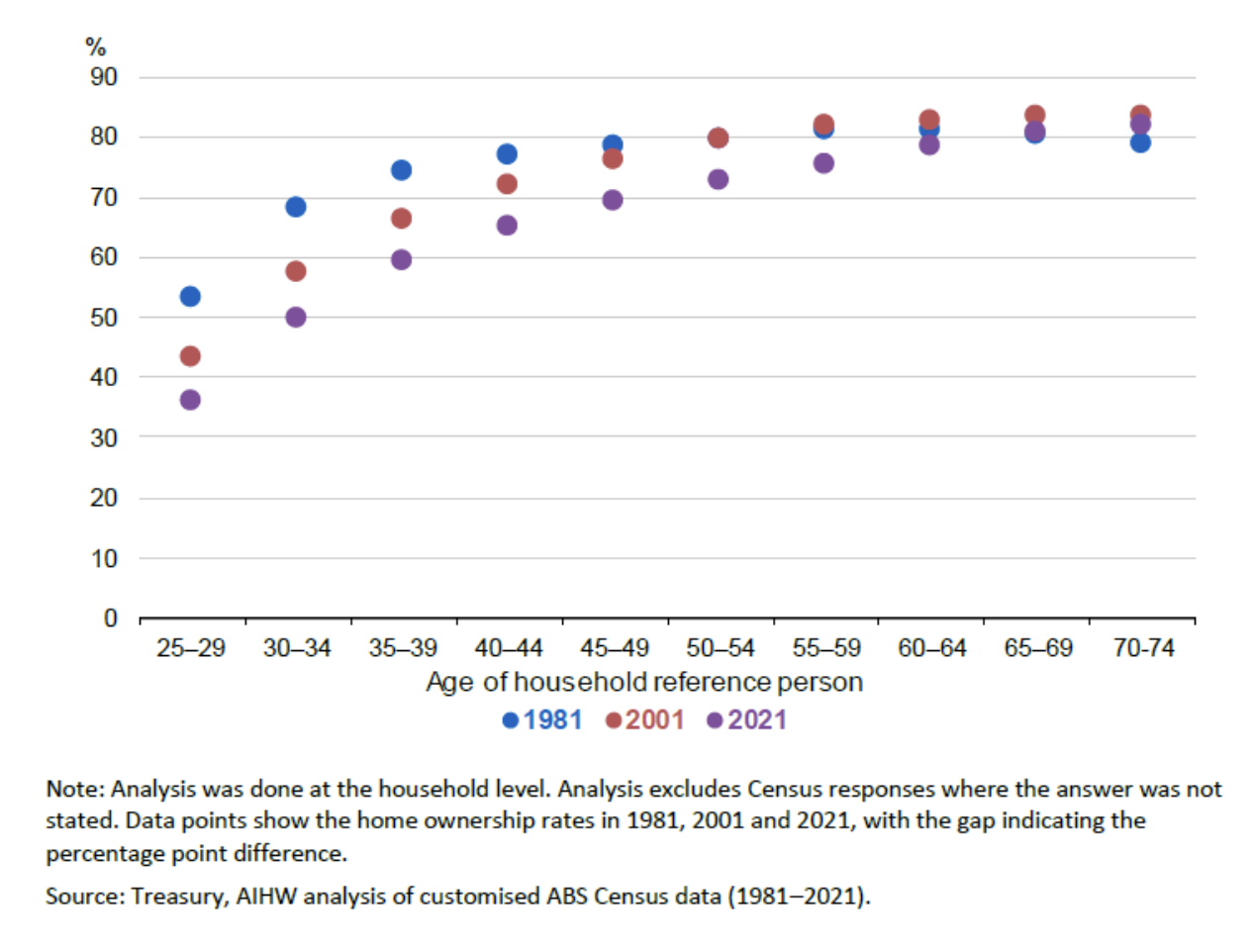

As now widely reported, this Budget will reduce the tax advantages residential property investors have experienced over the past 25-odd years. In so doing, it is aiming to reduce the ‘crowding out’ effect of higher-wealth, better-funded investors elbowing would-be first home buyers out of property ownership.

The Government is hoping to reverse a decade of decline in the rates of home ownership, with a fall of seven percentage points between 2001 and 2021 for households aged 25 to 34. The longer-term decline across different age groups is provided below, from the most recent Treasury Intergenerational Report.

The Budget estimates that some 75,000 new home-owning households could be created by the changes over a decade, relative to the status quo.

It also proposes to limit negative gearing for residential property investments only to new builds from 1 July 2027, and to allow property-related losses to only be deductible against other income from residential properties.

At present, investment property-related losses can be used to reduce other forms of taxable income, and is part of the reason why some of the most enthusiastic proponents of negatively gearing property include high-income earners such as surgeons, anaesthetists and other medical specialists.

Capital gains, productivity losses

As for capital gains, the Budget proposes to return to the pre-September 1999 regime of applying tax only to real, inflation-adjusted capital gains.

The 50% discount (for assets held for 12 months or more) was introduced in 1999 as a recommendation of the Ralph review into business taxation. It was justified as likely to stimulate investment in capital-intensive assets like plant, equipment and R&D; assets that increases productivity, and so Australia’s per capita income, over time.

With the benefit of hindsight, the animal spirits that were ignited by the 50% CGT discount were more enthusiastically directed into residential property investing which, other than at the margin, does little to lift Australia’s long-term productive capacity and household income growth.

Residential land may appreciate over time, but it does not by itself generate any economic output.

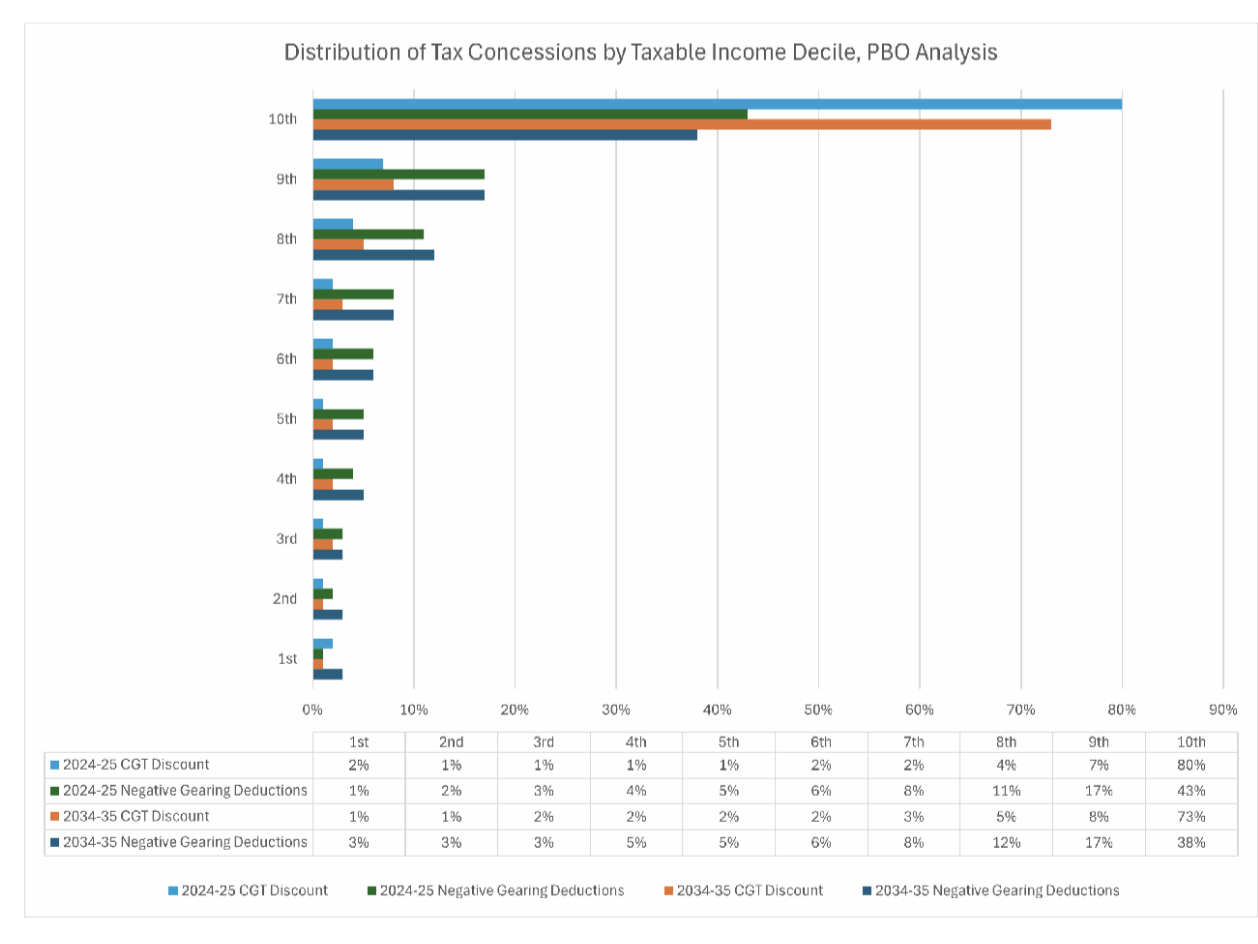

Previous analysis done by the Parliamentary Budget Office in 2024, from which I created the below chart, shows that 80% of estimated tax revenue foregone due to the CGT discount is captured by the top 10% of taxpayers, with these individuals also responsible for 43% of the revenue foregone due to negative gearing deductions.

A recent update by the PBO broadly reaffirms this analysis.

The Government is clearly hoping for a shift of individual investor preferences away from established residential property and toward new builds, and other economic activity, easing intergenerational inequity while lifting Australia’s woeful productivity position in the process. A two-for-one win, if successfully navigated.

Harry Chemay has more than two decades of experience across both wealth management and institutional asset consulting. An active participant within the wealth and superannuation space, Harry is a regular contributor to investment websites in Australia and overseas, writing on investing and financial planning.